Marcus Padley of Marcus Today says that there are income stocks, and there are stocks with high yields. What is the difference between income stocks, and stocks with high yields?

One of the traps for newer investors looking for income is to look at the size of the yield, rather than the reliability of the dividend stream.

Take two companies:

- The first has a share price of 100c, and it has a return on equity of around 10% (they make 10c a year for every dollar you give them), and that company pays a 10c dividend per annum which is 100% franked. On that basis, you get a 10% yield, and with an ROE of 10%, the company grows by 10% each year, taking the share price from 90c (after they go ex-dividend each year) back to 100c before they pay the next year’s dividend. This company offers a stable (the important bit) but low growth (and low risk) income stream of 10% plus franking. The perfect income stock. You don’t lose any capital and you get 10% plus franking every year.

- Now imagine another company that has a share price of 100c. But this company sells iron ore, and the iron ore price goes up and down all the time, and the company is never quite sure how much profit it is going to make. Sometimes it makes 20c a year in earnings, and sometimes it makes nothing. This company can’t be paying out dividends when it doesn’t make any money and can pay better dividends in a good year. So they decide that they will tell shareholders that their “dividend policy provides a minimum 50% payout of underlying attributable profit at every reporting period and that the Board will assess, every reporting period, the ability to pay amounts additional to the minimum payment, in accordance with the capital allocation framework”. You never quite know what dividend you’re going to get each year, but sometimes you get 20c, and it’s fully franked, but the next year you might get nothing.

So, which company do you buy if you want income from the stock market?

Well, it’s pretty obvious.

You have to live off your income, so you cannot be starved of income one year and hope that the next year they’ll make it up to you. You need reliability, and that is the essential ingredient of an income stock. Reliable income. Not income.

The dividend policy of the second company, by the way, is BHP Group Ltd’s (ASX: BHP) dividend policy.

The result is that companies that have unreliable earnings do not make reliable income stocks, and although some years everyone will be quoting the 13% yield on Fortescue Ltd (ASX: FMG), what they don’t tell you is that there is no guarantee they will repeat that next year, that the share price is extremely volatile, and that the share price will move more than the dividend multiple times a year, keeping you awake at night (which is an income stock fail).

And, that if you catch the wrong few years (BHP once underperformed for six years on the trot), the share price will chew up vastly more capital than you will ever get back in income.

Plus stocks that pay big dividends once, go ex-dividend harder than those that pay reliably.

It’s the ‘Yield Trap’.

If a company sells an asset and pays a huge one-off dividend, the moment the dividend is ‘ex’ the share price collapses rather than adjusts. Buying a stock for a big one-off forthcoming dividend can involve taking total return losses, even if you do collect the dividend and franking.

The bottom line is that for stocks like BHP, Rio Tinto Ltd (ASX: RIO) and FMG, even in the years that they yield 10%, the share price and share price volatility are much more important than the dividend, and rather than invest in these companies for income, you need to time these company share prices and hope they go up over the dividend period.

Sometimes you can get both – a run in the share price AND a big dividend. But you never ‘invest’ in these stocks for income. Their share prices will be as volatile as their earnings and dividends, which will depend on a volatile commodity price trend.

So if you want reliable, sleep-at-night income, you want to find boring, mature stocks with reliable, predictable earnings streams and nothing better to do with their earnings than to pay them back to shareholders as dividends.

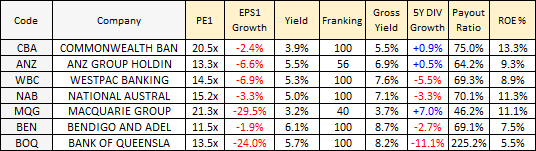

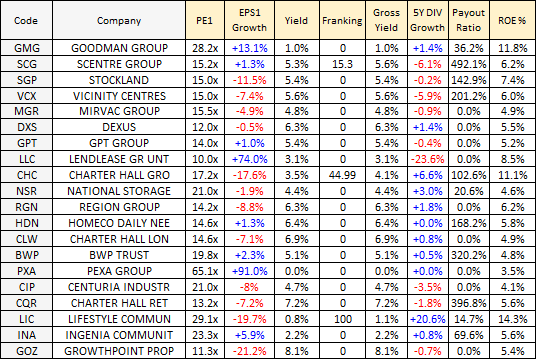

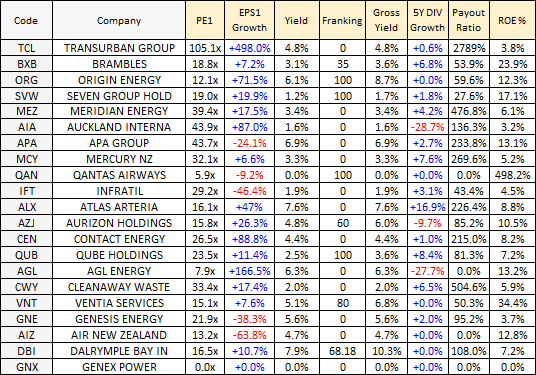

In Australia, you should look for stocks with high payout ratios (70% plus), yields of more than 4.5%, plus franking, a history of reliable dividends, and ROE of 5-15%.

3 obvious sectors in Australia that offer this

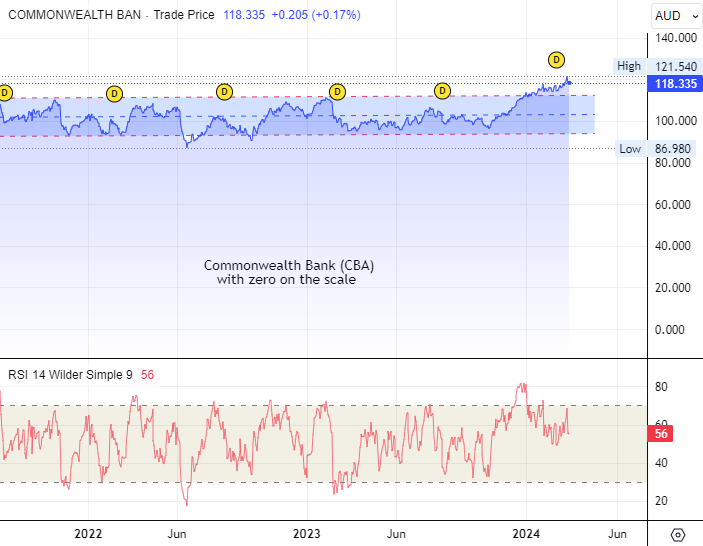

- Banks in Australia have an oligopoly because they have a captive population with very little competition. No international bank in its right mind would bother competing for the hearts and minds of 25 million Australians who are naturally suspicious, risk-averse and set in their ways. Trying to prise them away from their ‘bank for life’ is simply too hard when they can access a multiple of the Australian population in Europe, the US or Asia with far less effort. And are too big to be allowed to fail. They are low risk, ROE is 10-20%, and management feels a genuine responsibility to constantly increase dividends for their shareholders even when they can’t afford to. Only occasionally do the Australian banks threaten enough share price risk to be worth selling and buying back. Most recently during the GFC and then again during the Banking inquiry, both of which provided temporary but fabulous buying opportunities. The Australian banks are possibly the best income stocks in the world, and the top pick is the Commonwealth Bank of Australia (ASX: CBA) which has outperformed the other major High Street banks consistently over decades. The CBA is possibly the best income stock in the world. A pity it is expensive at the moment, but you have another six months until the next dividend to time your buying.

- REITs lend themselves to predictable earnings (renting out office or commercial factory space for ten years on a contract with set rental increases is very predictable) and, as such, lend themselves to very predictable ‘distributions’. Trusts have to distribute at least 90% of their earnings each year, hence the dividends are called distributions, and distributions at a trust level are not taxed so there are no franking credits. Trusts collect income and pass it on to investors. Income is then taxed in the investor’s hands at the investor’s tax rate. Your tax rate in your tax return. It’s very similar to getting a dividend plus the franking credit. REIT distributions just bypass paying tax first and recovering the franking later. So you need not be put off by there being no franking credit, there was no tax on the dividend to start with (on the distribution). Instead, you just compare the distribution without franking (the yield on a REIT) to the gross yield on other stocks (the yield including franking). Note that some REITs do have a level of franking; this will come from other businesses they own that are not under the REIT structure (trust structure), and those business units will be paying tax as normal, so there is some level of franking to come back.

- Utilities also make good income stocks because most offer essential services that do not see a lot of demand changes (Telecoms, power, water, gas) and have regulated prices that allow them a level of return that is fair – often 5-10%. That means they have very reliable cash flows whatever the economy is doing, and because of that, these companies can almost guarantee their return on equity and their dividends. They don’t grow much, but they always pay. You might have noticed over the years a series of Canadian Pension Funds buying Australian infrastructure and utility companies. Why? Because in Canada, they have the third largest pension plans, some pension funds pay 30-year annuities to their customers/members. The only way to meet those obligations is to buy companies that offer reliable earnings over long periods (30 years). The Canadian Pension Plan Investment Board (CPPIB) was part of the consortium to buy 51% of the WestConnex toll road project in Sydney worth A$9.26 billion. The Ontario Teachers’ Pension Plan and Caisse de dépôt et Placement du Québec have bought and bid for numerous listed and unlisted infrastructure assets in Australia, including buildings, airports, container ports and mobile towers. Canada’s Brookfield Asset Management spent $1.6 billion buying La Trobe Financial and $2.7 billion on Uniti Group (they also tried to buy Origin Energy Ltd (ASX: ORG) recently, I’m sure you remember). Because they, like you, appreciate the reliability of earnings. Note to self – the earnings numbers for Infrastructure and utility stocks are, in many cases, to be ignored – when you build a huge asset (a toll road), any earnings made are then met with enough depreciation and amortisation to reduce the earnings to close to zero so the company doesn’t pay tax. So the earnings can be non-existent and the PEs astronomical. So you have to look at another earnings number which is not generally obvious to make head or tail of ‘success’. The net result is that value investors using blinkered filtering of earnings never like utility and infrastructure stocks because the numbers are too complicated for them. So ignore anything earnings-related such as PE, payout ratio, and earnings growth.

But, finally, let me give you a final filter for a good income stock

It is this …

Put zero on the scale of the chart, and now look at the price.

What you should see is this:

One of the quirks of stock market charts is that almost all charting software is set to adjust the scale of the share price chart to fit all extremes over the set time period.

The net result is that very boring stocks that move in very tight ranges will look as volatile as volatile stocks.

But if you take into account the percentage movement on the chart, which is highlighted by putting zero on the scale, you may be able to pick up when a stock is a nice boring income stock, and when it is a volatile trading stock, that just happens to have a yield this year.

To make the point, here is the same chart of FMG with a zero on the scale. That rise from September last year to the January peak was 55.3%. It has just fallen 17%.

If it drops to the September low again it will be a 36% drop. If it drops to the 2022 low it will be a 53% drop. Who cares what the yield is? Get the share price wrong, and it doesn’t matter, all the dividend does is suck conservative income-focused investors into a volatile trading stock.

And the bigger the brand name (BHP), the safer you think it is, when it isn’t.

We just sold BHP and RIO (and last month sold FMG) in our portfolios because we think they are going down.

They are long-duration trading stocks that are coming off a good year and a high yield.

We hope to take advantage of their current downtrends to be able to pick them up at the bottom, not because they yield a lot, but because they are trading stocks not income stocks.