Yesterday, the information technology sector saw some large winners despite the continued sell-off of tech stocks in US markets in the previous trading day.

Two of the largest gainers yesterday were Altium Limited

(ASX: ALU) and Afterpay Ltd (ASX: APT), which finished the day up 6.6% and 7.6% up, respectively.

Taking a slightly more long-term view, however, both of these companies are still quite a way off from where they were in February. Altium’s and Afterpay’s shares are down 54% and 75%, respectively from their highs seen just a few months ago.

With both companies appearing to be trading at significant discounts, which is the better buy of the two?

Where has the growth come from?

Share price growth is one thing, but I’m also looking for companies that are able to demonstrate fundamental growth. In high-growth tech companies, sales (revenue) is often the go-to metric, as many of these companies aren’t generating earnings

(profit) yet.

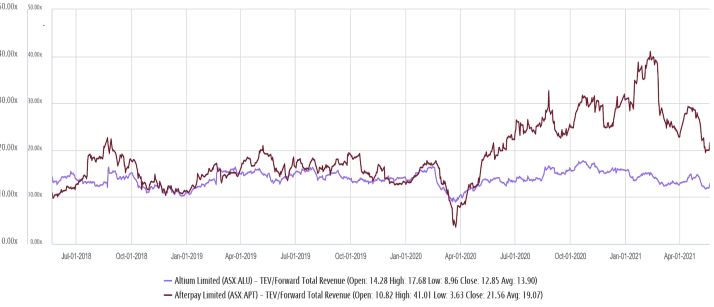

The below chart plots both Altium’s and Afterpay’s Enterprise Value (EV)/Sales ratio – Put simply, it shows the relationship between fundamental revenue growth and the price investors are willing to pay for its shares. So, if revenue and the share price were to increase at the same rate, the EV/Sales line should be horizontal.

While no one can doubt the extraordinary fundamental growth of Afterpay since the onset of the pandemic, it must be noted that the majority of shareholder returns during this time have been the result of investors simply paying a higher multiple for its shares.

Companies that trade on eye-watering multiples aren’t always a reason to avoid, but the implication is that the market is expecting high levels of growth in the future, which justify a higher valuation than normal.

My pick – Altium

Altium appears to offer a much better risk-return profile with less downside risk compared to Afterpay at these levels in my view.

Afterpay is clearly operating in a much larger addressable market, but I think its current valuation implies it’ll need to achieve high levels of fundamental growth to justify it.

On the other hand, Altium has definitely fallen out of favour with the market, but I think there’s some further upside potential on the cards.

Management has some bold plans to grow revenues to over US$500 million in five years (currently $189). While this isn’t a certainty, I feel like the downside risk of management failing to execute would be substantially less if the same were to happen with Afterpay.

That isn’t the only reason I like Altium though. You can read more about why in this article: The Altium (ASX: ALU) share price could be in the buy zone. Here’s why.

If you’re on the hunt for other ASX growth shares, I’d recommend signing up for a free Rask account to gain access to our stock reports.