There are a few ways to invest in shares and ETFs for kids in Australia, but the tax position varies:

- Investing in the parent’s or grandparent’s name, with the parent’s TFN quoted

- Investing in the parent’s name, as trustee for the child, with kid’s name and TFN noted

- Investing for the kid via a family trust

Each tax structure has pros and cons, but for most parents and grandparents, investing for kids in shares and ETFs is pretty straightforward.

💡 Want to invest for kids with us? Click here to start investing for kids (or grandkids) with Rask.

My advice: don’t get hung up on the tax structure, just get started, pick some growth ETFs or shares, contribute regularly, use the child’s TFN in most cases.

Here’s a detailed look at the options available when investing in shares and ETFs for kids.

Option 1: Investing in the parent’s name and TFN

First, the easy option: own the shares in your name and, when they’ve matured enough, gift them some money (my tip: set the expectation that they won’t be inheriting it, unless they prove their worthy of it).

As the ATO writes, “In Australia, gifts and inheritances are generally not considered as income and don’t require you to pay any Australian taxes.”

(Obviously, rules can change, and gifting may affect things like pension payments, but for the most part, it’s pretty straightforward.)

Option 2: parent is legal holder, kid is beneficial owner

A tactical (but still free!) options for people investing, say, $500 – $30,000 is to make the child the beneficial owner and allow them to be taxed

Here are a summary of choices:

#1 – Invest in your name (i.e. your own brokerage account, with your tax file number or TFN quoted – this may affect capital gains tax later on…)

#2 – Invest via your partner’s name (same thing, but under the partner’s name and TFN)

#3 – Hold the shares “as trustee for” the child (quoting their TFN)

Crucially, #3 is what gets people in a tizzy. “Who’s TFN do I use?”, “But will they pay tax at 18 when I transfer them the shares?”, and “who pays the tax on dividends between now and then?”

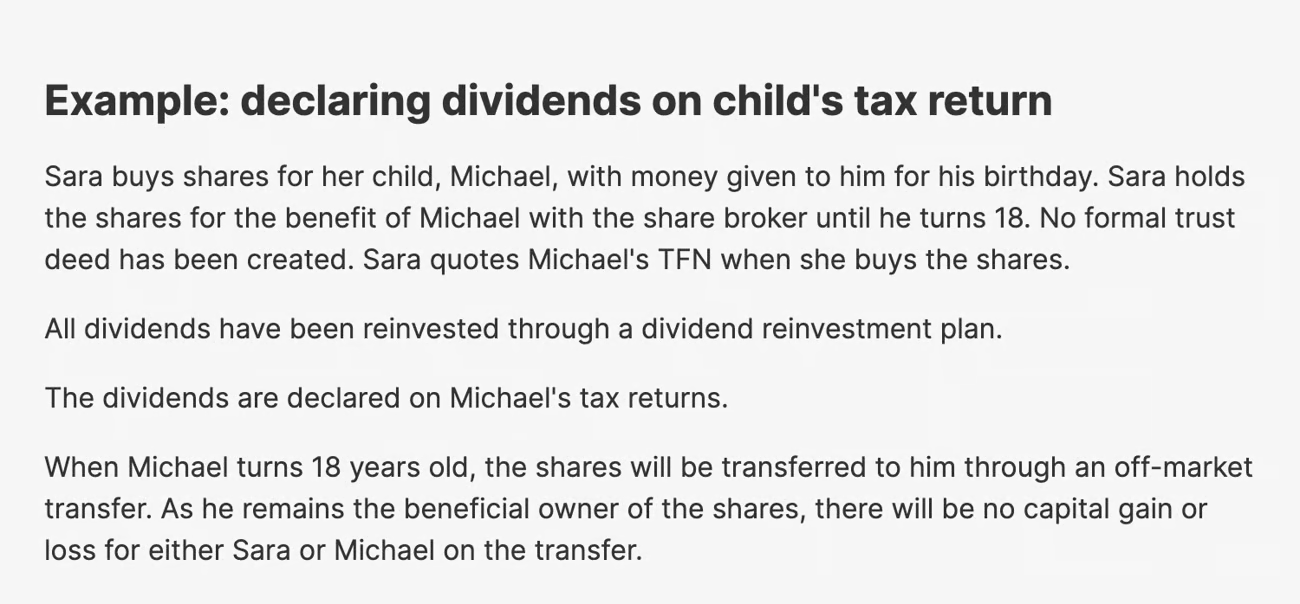

This ATO example taken straight from the website sums it up perfectly:

If you’re wondering, ‘this all sounds a little complicated’…

In Australia, as in many places around the world, kids cannot legally own shares/ETFs. However, they can have beneficial ownership. In other words, a parent/adult can legally hold the shares, on behalf of, and for the benefit of, the child.

The key is signalling to the ATO, when using your broker, that you’ve set it up right – and the child’s account is indeed properly managed, and taxed. Otherwise, you, or the child, might pay tax when they receive the shares.

For example, putting down the correct TFN on an investment account may seem like only a small thing, now, but it’s probably worth thinking about if the child is happy to cop the income tax to receive more shares later in life.

#1 – child’s TFN on the account means the child pays tax on the dividends, and should avoid CGT when shares are transferred to them.

When a child earns certain types of income, it can have the impact of incurring a meaty amount of tax on the dividends. But, seriously, I think parents and grandparents worry way too much about this.

According to the ATO website, a child pays higher rates of tax to avoid parent’s shovelling money into their tax return. For investment income over $416 per year, the child will pay 66% on the extra amount up to $1,307 per year. After that, it’s 45% – the same as a high income earner.

For example, a $10,000 Australian shares ETF could be paying 4% per year income. That’s $400. So, nil tax.

Another example… a $20,000 investment split 60% in US shares (S&P 500) and 40% Australian shares might pay ~$460 income. So, ~$29 in tax. In fewer words, “bugger all.”

As you can imagine, most people investing for their children don’t need to get all fancy or stressed out. Just cop the tax and move on. It’ll be more important to focus on which investments you should make (see below).

(Note: a child’s employment and other things are still taxed like normal, I’m simply talking about investment income).

#2 – adult’s TFN on the account means the adult pays the tax but it could have CGT implications.

For my young sister’s account (which has ~$800 in it), I hold her ETFs in my name, using my TFN – so I’m taxed. If she starts powering ahead with thousands upon thousands of contributions in her later teenage years, we’ll likely make use of her TFN.

(At 18, I’ll probably just gift her some cash for her birthday, and keep the current shares for myself anyway).

Option 3 – Family trust investing for kids

At the end of the day, someone is going to be paying tax, even if you use a family trust, which probably the most complex and costly of the strategies.

For the vast majority of people, Options #1 and Options #2 are fine.

But how about if you have lots of cash for the child’s account? Like, $500,000?

If you’re investing anything really meaningful ($500k was just an example), I’d always get expert tax advice from people who know how to structure investments for the long run.

When you speak to a tax accountant, or tax (financial) adviser, you can ask them things like:

- Is a family trust worth it for me/us?

- Should I have a bucket company?

- Can you tell me how investment bonds are taxed and if I could use one?

- Should my trust have a corporate trustee?

I definitely do not have $500,000 for a kids account. But going forward, I’ll be using a family trust for all of my investing because my situation involves a family business, stakes in other private businesses, personal investments, future planning for children, and so on.

This is unnecessary financial engineering for most people, but it’s what I have for my family.

A family trust is more costly than simply holding the shares as trustee for the benefit of child. A family trust setup can be up to $4,000. Then there’s yearly tax returns and ongoing fees adding up to, perhaps, $750 – $1,500.

I have incurred substantial costs over many years for my trust and company structures – with literally no benefit – but ultimately it is now starting to work in my favour.

To be clear: I wouldn’t consider a family trust unless you have a business, private investments, you’re concerned about legal risk (e.g. family home), or you are in need of much more flexibility. Get good advice before doing that.

Option 4 – Invest with Rask

If you want to take away nearly all of the complexity of investing for kids, you can invest for your kids with Rask. Our Rask Invest Luna strategy is designed for kids. Watch the video below, or click here to start investing for kids.

In summary, when investing for kids

- Simple and very good: it’s the parent’s account held as trustee for the benefit of the child (with their TFN, for CGT transfer reasons). Stick to high growth investments like our Jupiter strategy or Luna. Most platforms will have options for “minor” or “kids accounts”.

- More complicated families: use a family trust, in consultation with an account or adviser.

If you want to explore this topic further, here are some resources:

- This lovely community discussion about investing for kids, started by Mitchell.

- This weekend’s Australian Investors Podcast 2 Sense edition, in which financial adviser Drew Meredith and I discuss the confusion about TFNs and parent’s names.

- This week’s LIVE show with Pearler’s Ana Kresina, author of Kids Ain’t Cheap. My internet may have dropped out momentarily but Ana succinctly explained the keys to thinking about the next generation and how it’s commonly done.