WiseTech Global Ltd (ASX: WTC) has become one of the most fascinating stocks on the ASX. At least, I think so. That’s why I own shares.

It’s not because the WiseTech business is simple.

It isn’t.

Not because the valuation is easy.

It definitely isn’t.

And not because the WiseTech share price has been kind to investors recently.

It hasn’t.

WiseTech has been caught in the middle of several market fears at once: the so-called SaaS apocalypse, AI disruption, governance concerns, a major US acquisition, customer pushback on pricing, and investor anxiety about whether CargoWise can keep growing like it has in the past.

That’s a lot of baggage.

But sometimes baggage is where opportunity hides.

The big question for investors is not whether AI changes software.

Of course it does.

The better question is:

Can AI actually replace CargoWise, the logistics software platform that sits at the centre of WiseTech Global’s business?

I don’t think that question has a simple answer.

But I do think the market may be making a lazy assumption.

AI can write code.

That does not mean AI can instantly recreate decades of logistics workflows, customs rules, compliance checks, documentation, integrations, customer data, global trade knowledge, bureaucratic approvals and industry trust.

That distinction matters.

A lot.

What does WiseTech Global Ltd (ASX: WTC) actually do?

WiseTech Global is an Australian software company focused on global logistics and trade.

Its core product is CargoWise.

CargoWise is used by freight forwarders, customs brokers, warehouse operators, transport businesses and logistics service providers to move goods around the world.

That sounds boring.

Good.

Boring is often where the money is.

CargoWise helps logistics companies manage things like:

- international freight forwarding

- customs declarations

- trade compliance

- shipment tracking

- documentation

- warehousing

- invoicing

- transport movements

- customer communication

- regulatory workflows

In simple terms, CargoWise helps a logistics business answer questions like:

Where is the shipment?

What documents are missing?

Has customs cleared it?

Who needs to be billed?

Which carrier is moving it?

Is the importer/exporter compliant?

What happens next?

That might not sound sexy.

But if you are moving millions of containers, air freight shipments or customs declarations across dozens of countries, it is mission-critical.

CargoWise is not a nice-to-have productivity app.

It is much closer to the operating system of a freight forwarding business.

If it goes down, the business has a problem.

If it works well, the business can process more shipments, reduce manual labour, lower compliance risk and serve customers more efficiently.

This is the part many investors miss.

WiseTech is not “selling software”.

It is selling throughput, compliance and operational leverage.

The origin story: from freight forwarding software to global trade infrastructure

WiseTech was founded by Richard White and Maree Isaacs in Sydney. I interviewed Richard in a rare, very long-form interview. This was recorded before the WiseTech share price sell-off and Fairfax articles emerged.

The company started by building software for Australian freight forwarders. The original opportunity was narrow: help logistics businesses replace messy, manual, disconnected systems with software that could actually handle the complexity of freight forwarding.

But freight forwarding is not just an Australian problem.

It is a global problem.

The same issues exist everywhere:

- fragmented systems

- duplicate data entry

- customs complexity

- poor visibility

- manual documentation

- inefficient workflows

- operational risk

WiseTech’s ambition grew from serving local freight forwarders to building what management now calls the operating system for global trade and logistics.

That sounds like a big claim.

Maybe too big.

But it is useful because it tells us how management thinks.

WiseTech does not want CargoWise to be one module in a logistics company’s tech stack.

It wants CargoWise to be the system around which the logistics business runs.

That is the foundation of the bull case.

It is also the foundation of the risk.

When a company is trying to become this important, investors need to ask whether the moat is real — or whether the market has simply fallen in love with a story. Usually, I want to see a “moat attack” play out in real life…

Why CargoWise became so sticky

The best way to understand WiseTech is to stop thinking about software features and start thinking about workflow.

A freight forwarder does not just “use” CargoWise.

The business can be built around it.

A shipment may touch sales, operations, customs, finance, customer service, warehousing, transport and reporting. If all of those steps are inside CargoWise, the software becomes deeply embedded.

That creates switching costs.

Not switching costs in the lazy textbook sense.

Real switching costs.

The kind where changing software can mean:

- retraining staff

- migrating sensitive customer data

- rebuilding integrations

- changing operational processes

- re-testing compliance workflows

- disrupting billing

- risking customer service failures

- reworking reporting

- reconnecting with partners, carriers, customs systems and customers

This is not the same as switching from one project management app to another. I see this playing out time and time again with analysts and investors who don’t understand the business side of investing well enough.

CargoWise lives inside complicated, regulated, high-volume workflows.

That is why I think the “AI kills software” argument is too simplistic.

AI may make software development easier.

But CargoWise is not valuable only because WiseTech employees wrote code.

It is valuable because the code is wrapped around 30 years of logistics knowledge, product iteration, customer implementation, data, integrations and trust.

That is much harder to replicate.

Who competes with WiseTech?

WiseTech does not operate in a vacuum.

CargoWise competes against a mix of specialist logistics software, global enterprise platforms, internal systems and increasingly AI-enabled workflow tools.

The competitor set includes:

- Descartes Systems

- SAP

- Oracle

- Blue Yonder

- Manhattan Associates

- Magaya

- GoFreight

- internal freight forwarder systems

- AI workflow automation start-ups

There are also adjacent ASX-listed quality software and platform businesses investors often compare with WiseTech, including Pro Medicus Ltd (ASX: PME), Xero Ltd (ASX: XRO), TechnologyOne Ltd (ASX: TNE) and REA Group Ltd (ASX: REA).

Those businesses are direct competitors, but simply ‘peers’ in the tech sector listed on the ASX. So, at best, they help frame the investment question and the valuation investors are willing to place on the ASX’s best tech companies.

So, what do the best Australian software/platform companies have in common?

Usually:

- recurring revenue

- strong margins

- high customer retention

- deep workflow integration

- pricing power

- large addressable markets

- product-led cultures

- long reinvestment runways

WiseTech has many of those ingredients.

The debate is whether the recent risks have damaged them.

Why the WiseTech share price has been smashed

The WiseTech share price has not fallen because investors suddenly discovered logistics is difficult.

That was always true.

The share price has been hit because multiple concerns arrived at once.

First, AI.

Investors are worried that AI will make software cheaper to build and easier to replicate.

Second, governance.

WiseTech has been dealing with ongoing controversy and media attention involving founder Richard White. I’m not going to replay those allegations here. That is not the point of this article and I think WiseTech (with its thousands of employees) is now bigger than one person.

That said, when a founder is perceived to be central to product vision, culture and capital allocation, governance noise can become valuation noise.

Third, the e2open acquisition.

WiseTech completed a large US acquisition that materially expands its market opportunity, but also adds debt, complexity and integration risk.

Fourth, the new CargoWise Value Packs.

WiseTech has shifted CargoWise away from seat-based pricing and towards transaction-based pricing. Strategically, I think this makes sense in an AI world. But it is also a major commercial change, and customers do not always love major commercial changes. It can create a ‘churn event’ because a customer reviews what’s on offer before committing – potentially for the first time in a while.

Fifth, organic growth.

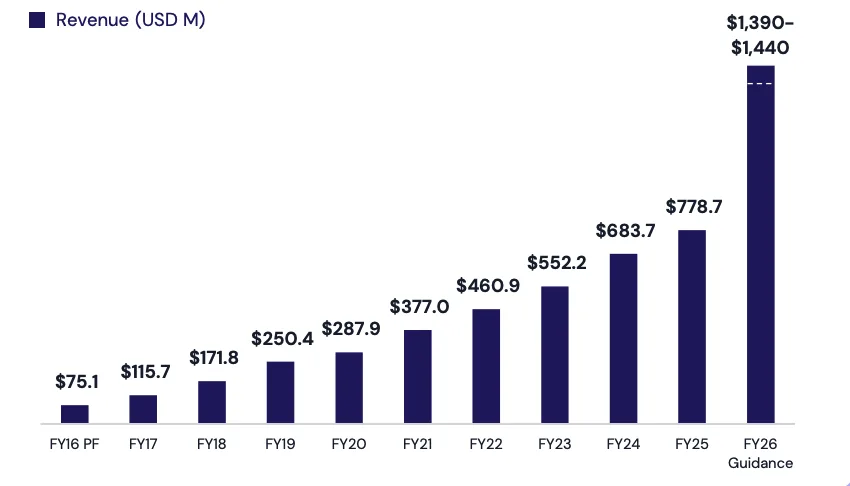

The headline revenue growth looks spectacular because of e2open. But investors should still pay very close attention to organic CargoWise growth. The most recent organic figure was 9% growth year over year.

In software, acquisition-led growth is fine – so long as it reinforces the competitive advantage.

But organic product-led growth is better.

The new commercial model: clever, risky, or both?

WiseTech’s new CargoWise Value Packs may be one of the most important parts of the investment case.

The company is removing seat fees and standard cloud hosting fees and moving customers towards transaction-based pricing.

That matters because AI may reduce the number of humans needed inside logistics businesses.

If WiseTech continued to charge mainly by user seats, and AI helped its customers reduce headcount, WiseTech could accidentally reduce its own revenue.

That would be bad.

By charging based on transactions instead, WiseTech is trying to align revenue with customer throughput.

More shipments.

More customs declarations.

More activity.

More value.

More revenue.

In theory, this is smart.

Very smart.

It also helps minimise competition entering the market – because existing customers have lesser reason to switch for price savings and competitors weighing up whether to spend big on capex and replicate WiseTech face an NPV problem (the investment might not stack up).

But here is the catch.

Commercial model changes can be noisy.

WiseTech says most CargoWise customers have moved to the new model, but the remaining customers include many of the largest customers on longer-term agreements. These 5% of customers represent a meaningful chunk of CargoWise revenue – estimated to be as much as 20%.

That means the biggest prize is still partly ahead.

The bull case says those large customers will eventually move to WiseTech’s new pricing because the AI functionality and productivity benefits are too valuable to ignore.

The bear case says the process may be slower, more painful and more competitive than investors expect.

Both arguments are reasonable.

Can AI replace CargoWise?

This is the heart of my research.

Can AI replace CargoWise?

My answer: probably not easily.

But AI can absolutely attack parts of the workflow.

That nuance matters.

AI can already help with:

- document ingestion

- invoice processing

- customs classification

- restricted party screening

- customer support

- workflow automation

- code generation

- testing

- translation

- data extraction

- exception handling

WiseTech itself is proving this.

The company has launched AI tools for document ingestion, compliance risk screening, classification assistance and customer/product support.

That tells us two things.

First, AI is real.

Second, WiseTech is not sitting still.

The important distinction is between AI as an external overlay and AI embedded inside the core workflow.

An external AI tool might help a user extract data from a PDF or automate a few clicks.

Useful?

Yes.

Disruptive?

Potentially.

But embedded AI inside CargoWise is different.

If the AI can access the workflow, understand the data, follow the operating rules, communicate with the right systems, respect permissions, support audit trails and work inside the system of record, it becomes far more powerful. It could be the difference between switching your company from Microsoft 365 to Claude, versus just using Copilot (ChatGPT inside Microsoft).

That is WiseTech’s argument.

And I think it has merit.

CargoWise is not simply a spreadsheet with a nicer interface.

It is a regulated logistics workflow engine.

That is much harder to vibe-code.

The strongest AI bear case

Let’s get real.

AI is a real threat.

The strongest bear case is not that ChatGPT launches “CargoWise 2.0” next week.

That is silly.

The stronger bear case is that AI slowly reduces the advantage of incumbency.

For example:

- smaller competitors may build better features faster

- customers may automate workflows around CargoWise

- large freight forwarders may improve internal systems

- migration may become easier over time

- AI-native tools may win specific workflows

- pricing power may weaken if customers think software is less scarce

- implementation and support may become less differentiated

That is the real risk.

AI does not need to kill CargoWise overnight to hurt WiseTech’s valuation.

It only needs to reduce the market’s confidence in CargoWise’s growth, pricing power or durability.

When a stock trades on high expectations, even small changes in confidence can move the share price dramatically.

The strongest AI bull case

The strongest bull case is that AI actually strengthens WiseTech.

Why?

Because WiseTech has:

- the existing customer relationships

- the workflow

- the data

- the integrations

- the compliance content

- the domain expertise

- the system of record

- the balance sheet to invest

- the installed base to distribute AI features

In this scenario, AI makes CargoWise more valuable, not less.

Customers process more freight with fewer people.

Compliance improves.

Manual data entry falls.

Support costs decline.

WiseTech’s own software development becomes more productive.

Margins improve.

The product gets better faster.

That is the dream.

And, to be fair, it is not an unreasonable dream.

The company has already said it expects AI to structurally reshape its cost base, including significant reductions across product, development and customer service roles.

That sounds brutal.

But from a shareholder perspective, it may be powerful if — and only if — product quality does not suffer.

That is the key.

Cutting costs is easy.

Cutting costs while improving product velocity is much harder.

The e2open acquisition: brilliant or messy?

I reckon WiseTech’s acquisition of e2open is a massive swing. While they’ve done many acquisitions before, this was a big one.

The strategic logic is obvious.

Historically, WiseTech was strongest in logistics execution: freight forwarders, customs brokers and logistics service providers.

e2open expands WiseTech into broader supply chain software, including manufacturers, brand owners, importers, exporters, carriers and supply chain planning.

In plain English, CargoWise helps move the goods.

e2open helps connect more of the supply chain around those goods.

That could be powerful.

If WiseTech can connect logistics execution, trade compliance, supply chain planning, electronic bills of lading, carrier networks and customer workflows, the long-term opportunity becomes much larger.

But I do not want to gloss over the risk.

Big acquisitions are hard.

Big US software acquisitions are harder.

Big US software acquisitions while changing your commercial model, restructuring with AI, managing governance issues and launching a new container optimisation product are harder again.

e2open also appears to bring lower margins, more professional services revenue, customer attrition to work through, and a business that management wants to shift from sales-led to product-led.

That may create value.

But it requires execution.

Lots of it.

Container Transport Optimisation: potentially huge, but early

Container Transport Optimisation, or CTO, is another fascinating part of WiseTech that no-one in the investment community seems to talk about.

The idea is to reduce inefficiency in container transport.

Today, trucks often move containers through ports, transport yards, importers, exporters and empty container parks in inefficient patterns. There are dead legs, duplicated movements, unnecessary storage and poor system-wide optimisation.

WiseTech wants CTO to optimise the whole system, not just one participant’s local problem.

That could reduce:

- empty truck movements

- container park visits

- storage costs

- handling costs

- fuel usage

- emissions

- road congestion

- wasted labour

The opportunity could be enormous.

But it is still early.

Management has made clear CTO is being implemented with ACFS in Australia. It is not yet broadly proven at global scale.

This matters.

Investors should not value CTO as if it is already a mature global revenue engine.

It is more like a highly valuable call option.

If it works, it could be massive. Like Waymo, for Alphabet/Google.

If it takes longer than expected, it may remain more promise than profit for a while.

You value WiseTech’s existing business and if CTO pays off, great. If not, it doesn’t change the margin of safety. It’s the cherry on the cake – with or without it, it should be yummy.

WiseTech’s moat: where I think it is real

I think WiseTech’s moat is real.

But I do not think every part of the moat is equally strong.

Here is how I’d break it down.

Switching costs: very strong.

Once CargoWise is embedded into operations, replacing it is painful.

Regulatory complexity: very strong.

Customs, sanctions, documentation, trade compliance and jurisdiction-specific rules are not simple problems.

Workflow depth: very strong.

CargoWise touches many parts of a logistics business.

Integrations: strong.

Connections to carriers, ports, customs systems, customers and internal workflows matter.

Brand and trust: moderate/strong.

Large global logistics businesses do not pick core systems lightly.

Data advantage: potentially strong.

But only if the data is usable, permissioned, structured and embedded into workflows.

Network effects: moderate.

There is ecosystem value, but I would not call this a classic marketplace network effect.

Founder/product culture: historically strong.

But also a governance and key-person risk if not managed carefully – as we’ve seen play out.

ACCC: investors should not ignore this

One interesting data point is the ACCC’s view on WiseTech’s position in Australian logistics software.

The ACCC required WiseTech to divest Expedient after its e2open acquisition, saying WiseTech already had substantial market power in Australian logistics software.

That is both bullish and bearish.

Bullish because regulators do not usually worry about companies with weak market positions.

Bearish because market power attracts scrutiny, and pricing changes can attract customer and regulatory attention.

This is one of those rare situations where the same fact supports both sides of the thesis.

Strong moat.

Higher scrutiny.

What investors should watch from here

I would not judge WiseTech on one metric.

I would judge it on a handful of long-term indicators – many of which will show up as the company continues to report official results (2026 is a big year for WiseTech!).

The most important ones are:

- CargoWise organic revenue growth – obvious.

- adoption of CargoWise Value Packs – what adoption and usage like? Short-term dips in revenue are okay.

- large customer transitions – what does it mean in revenue terms?

- customer retention

- e2open integration progress – cost savings or revenue expansion?

- e2open margin improvement

- CTO proof points – any solid commentary on this would be good, but it’s not core to an investment thesis.

- AI product adoption

- software development productivity

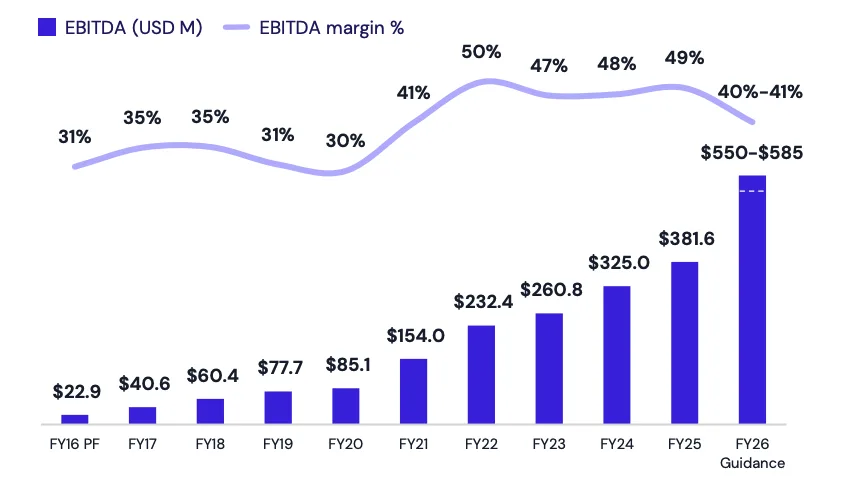

- gross margin and EBITDA margin recovery – analysts are expecting a lot because the company has promised them something good.

- balance sheet deleveraging – the debt associated with e2open might be okay for now, if cashflow-to-debt ratios are solid.

- governance stability

For me, the most important metric is still organic CargoWise revenue growth. While all of them matter, the business model boils down to this as the most important.

If CargoWise can keep growing organically while WiseTech improves margins and integrates e2open, the bull case gets much stronger and the stock will pop big time (if I was to guess – short-term predictions are a mug’s game).

If organic growth slows and the company relies heavily on acquisitions, pricing and cost cuts, the market will probably stay sceptical.

Valuation: what should investors focus on?

I’m not going to pretend I can perfectly value WiseTech here. But it looks cheap. On a price-to-revenue (P/S) basis, it’s the cheapest it’s ever been.

But the share price moves quickly. Analyst forecasts change during uncertainty (because sell-side analysts are lemmings). From there, multiples compress and expand. Markets throw tantrums. Spreadsheets lie with confidence.

But I do know what I would focus on to get comfort that it is indeed cheap and the valuation could expand as profits grow…

For a company like WiseTech, valuation should be judged against:

- recurring revenue growth

- organic CargoWise growth

- gross margin

- EBITDA margin

- free cash flow conversion

- return on invested capital

- net debt and deleveraging

- customer retention

- reinvestment runway

- pricing power

The danger with high-quality software companies is that investors can overpay for perfection.

The danger after a sell-off is that investors assume the story is broken when it may only be wounded.

That is where WiseTech sits today.

Wounded?

Yes.

Broken?

I’m not convinced. At these prices, if organic growth can be sustained, I think investors would be buying with a margin of safety. But a lot can change.

Buy, hold or sell?

I’ll put it this way.

I would not buy WiseTech simply because the WiseTech share price has fallen.

Falling share prices are not automatically bargains.

Sometimes they are warnings.

But I also would not dismiss WiseTech because “AI kills SaaS”.

That is too lazy and even great businesses suffer moat attacks (remember Google and ChatGPT, Apple transitioning away from iPhones, and so on).

WiseTech may be one of the few ASX software companies where AI could strengthen the core business, provided management executes well.

CargoWise is deeply embedded. The customer problems are real.

But this is not risk-free.

Investors are being asked to underwrite a lot at once:

- a new commercial model

- AI-led restructuring

- e2open integration

- CTO commercialisation

- large customer conversion

- governance stabilisation

- continued organic CargoWise growth

That is a big list.

If management executes, WiseTech could remain one of Australia’s great global software companies.

If two or three of those things go wrong at the same time, the moat may still be real, but the valuation may not be protected.

That is the game for shareholders (like me) or new investors taking a look.

Final thought on WiseTech

I think the most interesting thing about WiseTech Global Ltd (ASX: WTC) today is that the market may be asking the wrong question.

The question is not: Will AI change software? Of course it will.

The question is: Does AI make CargoWise less valuable — or more valuable?

If CargoWise were just code, I’d be nervous. But CargoWise is not just code.

That is why WiseTech remains one of the most fascinating companies on the ASX.

Not because the story is clean.

But because the story is messy, important and potentially very mispriced.

For long-term investors who can tolerate volatility, WiseTech deserves a spot on the watchlist at least.

Maybe even more than that. I’ve added it to my portfolio (before the falls!) and to my Rask watchlist.