Reinvesting dividends can compound wealth, but it is not always the best move.

As the dust settles post-earnings season, investors turn their attention to what’s next.

Companies declared plenty of dividends, and with the cash due for payment spread out over the next few weeks, the question for shareholders becomes: take the cash or reinvest via a dividend reinvestment plan (DRP). DRPs automatically use your dividend to buy additional shares, sometimes at a small discount, and can be a powerful tool, compounding wealth over time.

You can take our dividend and DRP course here.

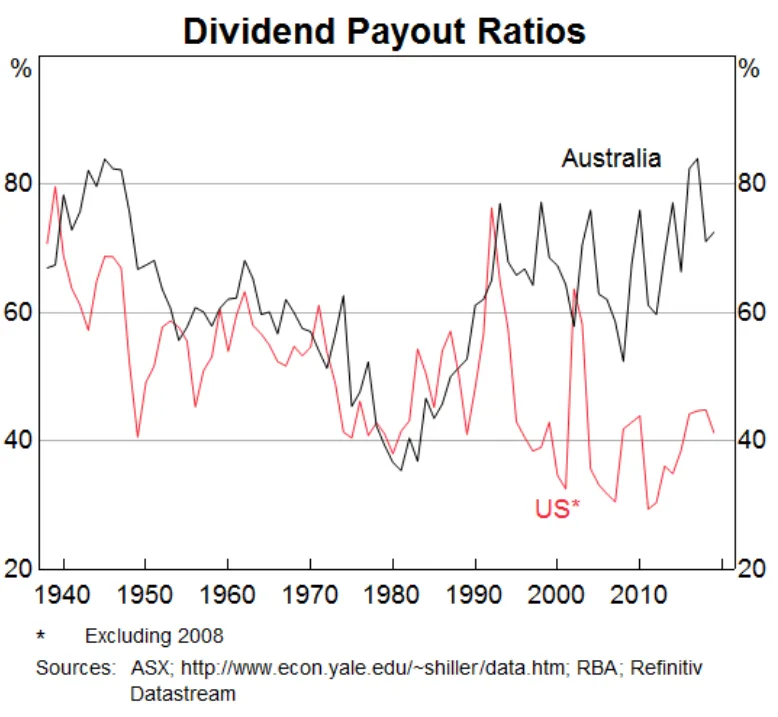

Reinvesting your dividends gives you more shares, which in turn generate their own dividends, creating a snowball effect and enhancing long‑term returns. In fact, thanks to Australia’s franking credit rules, the dividend payout ratio is much higher than that of global markets and makes up a large proportion of total returns. You can see in the graph below from the RBA that, following the introduction of franking credits in 1987, the ratios diverge; dividend payments in Australia have remained very high even as they have declined in the United States, likely reflecting their tax treatment here.

Seems like a no-brainer, right?

Are DRPs the best option?

Not always.

The primary downside is concentration risk. If you’re already heavily invested in a single ETF or company, reinvesting dividends increases your exposure to that position. Using DRPs across your entire portfolio could leave you over‑exposed in a handful of holdings. Access to cash also plays a role. DRP’s lock your capital away and should you need cash for a home deposit or emergency, having to sell holdings can be costly from a return and tax point of view.

As they say, cash is king.

I’m not getting cash, am I still taxed?

Firstly, speak to your accountant.

Even if you reinvest a dividend, the Australian Tax Office still treats reinvested dividends as income, so be prepared to pay tax on the dividends.

What about franking credits? These still apply; Australian companies often attach franking (imputation) credits to dividends, which represent tax paid at the company level. When you reinvest dividends, you still receive these credits, which can reduce your tax bill.

So while you’re not receiving cash, the reinvested dividend amount forms part of the cost base for the new shares. It’s important to keep accurate records of each reinvestment because each parcel of shares has its own cost base for capital gains tax purposes.

This record‑keeping can become complex if you participate in multiple DRPs across different stocks. Perhaps worth considering Navexa to help keep track.

So when should you use a DRP?

Like 95% of investing, it’s tailored to you and depends on your financial situation and goals.

An investor with a long-term view and comfortable with their portfolio mix can benefit from compounding via DRPs. This is especially true if the company or ETF trades below your estimate of intrinsic value. Those nearing retirement or who have significant holdings in the company may prefer to take the cash and allocate it elsewhere. This comes down to your preferred portfolio allocation.

Some companies don’t offer a DRP, so you may not have a choice. Others can offer discounted DRPs as an incentive, issuing shares at a price below the market. If a company’s share price appears overvalued relative to fundamentals, taking a DRP could mean buying at a high price. In such cases, it may be better to take the dividend in cash and invest in more attractively priced opportunities. It’s also key to read the documentation, and ensure you have elected to opt in to the DRP program prior to the election cut-off date.

The Rask recap

At the end of the day, the decision isn’t either/or.

You can elect to reinvest dividends for some holdings while taking cash from others. Thoughtful deployment of dividends ensures that your portfolio continues to grow while meeting your income and diversification needs.

Review each holding individually, consider your tax situation and future cash needs, and decide whether reinvesting or taking cash better advances your financial plan.