If you were to tell me that Sam Altman was developing an AI traffic cop:

- I’d believe you

- I would picture Arnold as the Terminator on every corner

- I wouldn’t believe two similar small-cap companies already trade on the ASX.

Introducing Smart Parking (ASX: SPZ) and Acusensus (ASX: ACE). Two growing companies at the smaller end of the market, developing technology to change the behaviour of parkers and drivers, with differing business models using sensors, software and machine learning.

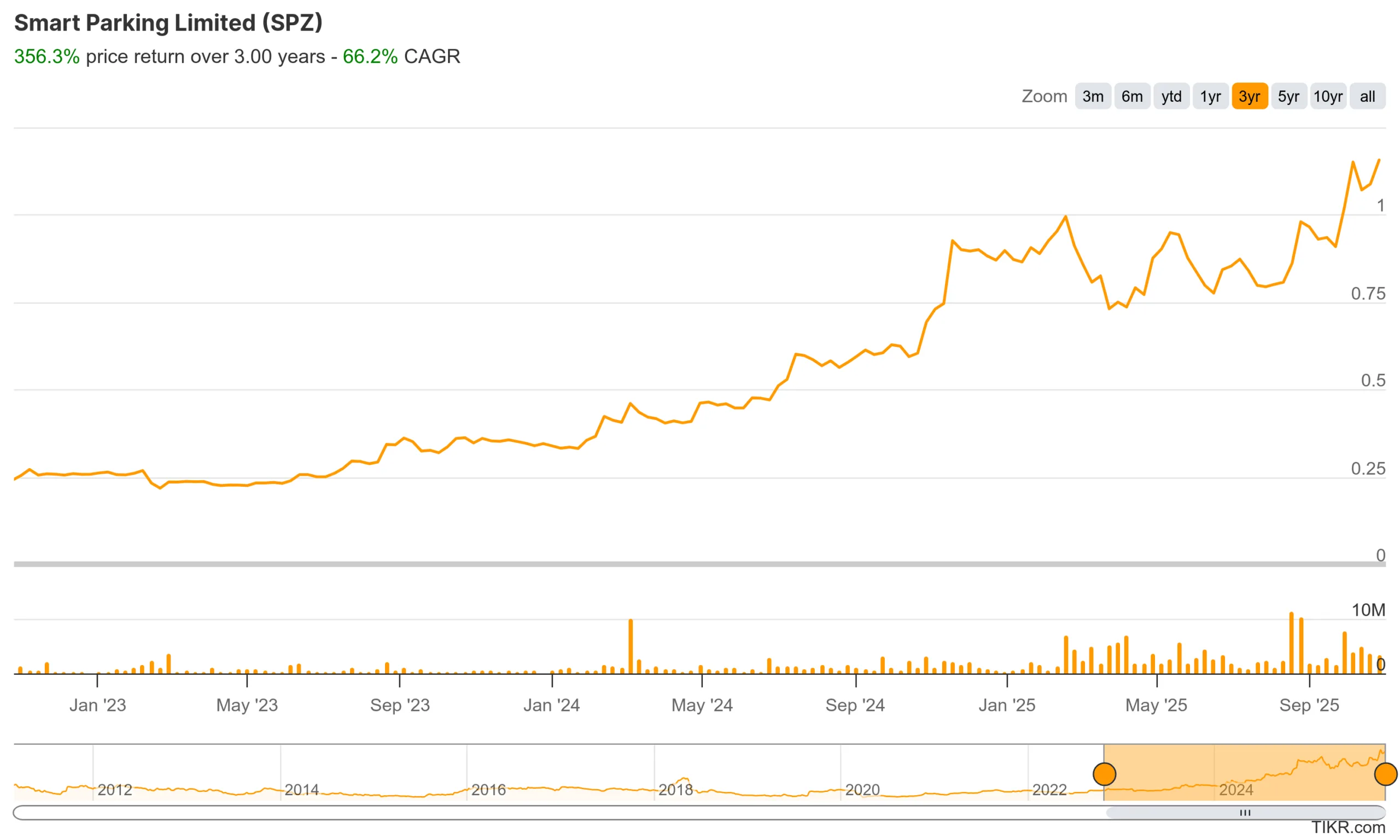

Smart Parking: The AI private car park inspector

Nobody likes parking inspectors (sorry to those reading this!)

The good news for commuters is that Smart Parking’s technology eliminates the need for parking inspectors! The bad news for those overstaying their welcome is that Automatic Number Plate Recognition (ANPR) cameras replace them. In English, the $450 million market cap’d company’s technology reads plates and uses its in-house cloud technology to detect whether a car has overstayed, and issues parking breach notices (PBN’s). In most cases, Smart Parking collects the entire PBN, on the odd occasion, it has a revenue share with the private park owner. This helps free up car parks within facilities and ultimately helps the owner with customer flow.

Adding sites and growing revenue

In many cases, Smart Parking will bear the cost of installing the cameras and collect the PBN’s which tend to deliver a quick payback.

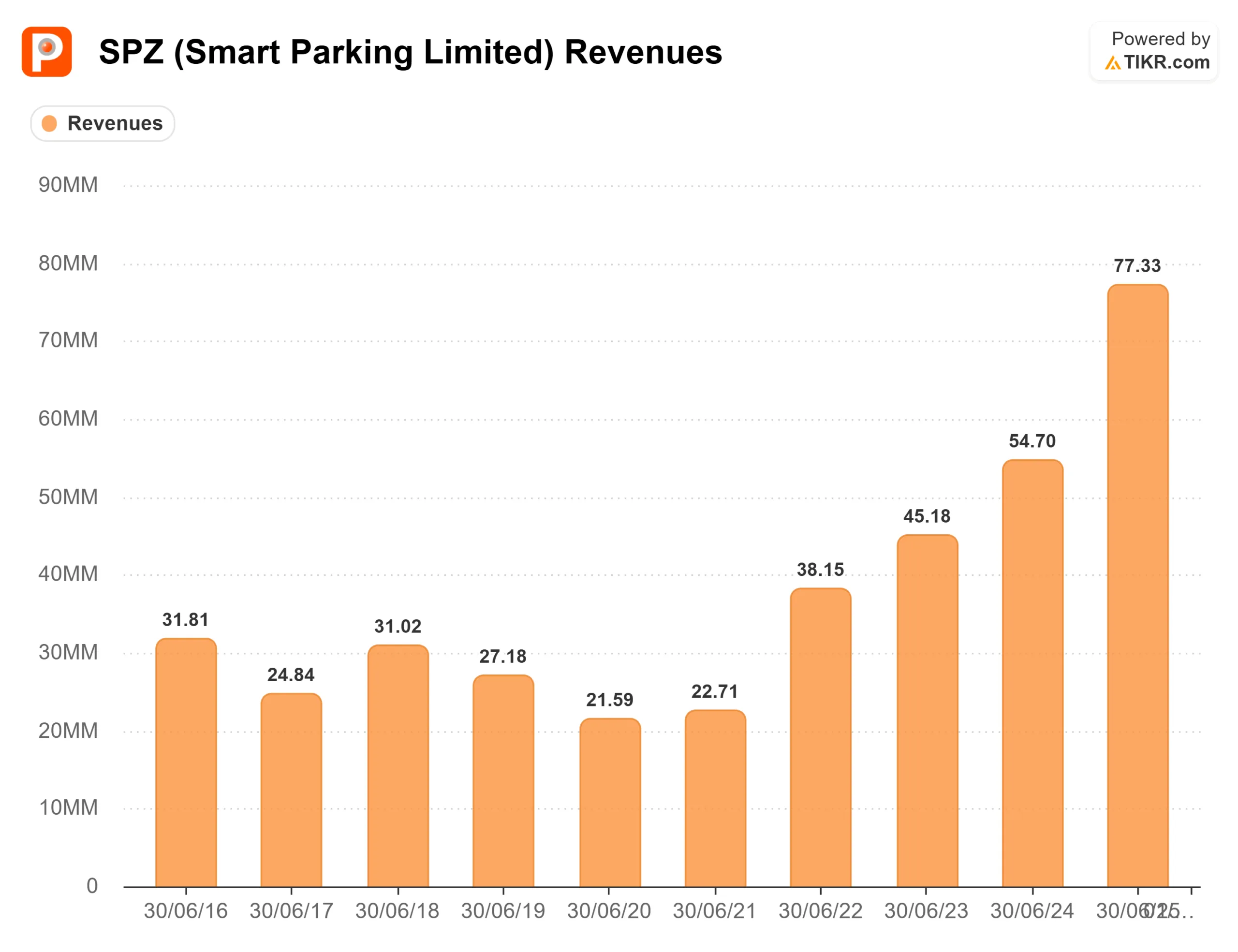

The company’s strategy has been to acquire sites, switch on cameras and collect PBN’s. Having a dominant position in the UK, the company has begun accelerating growth by acquiring operators in different geographies. This includes Germany, New Zealand, Denmark, and, more recently, the US. As of FY2025, the company managed 1,799 global sites, with a long-term target of 3,000 by December 2028.

PBN’s make up 98% of Smart Parking’s revenue, with the small balance comes from hardware.

Revenue has grown as the company acquires more sites and collects PBN’s.

It’s not all sunshine and rainbows.

Data collection companies are always at risk of leaks or government intervention. Smart Parking relies on access to driver registration data to issue and collect PBN’s. Without this, it’s difficult to collect 98% of the company’s revenues! We’ve seen Smart Parking pull the pin on its Australian venture. The Queensland government is putting a stop to data collection and effectively making the Aussie segment worthless. Consumer issues forced the UK also began tweaking its private parking code, looking to raise standards and potentially cap fines. This seems to have gone smoothly for Smart Parking after some initial fear showed up in the share price. The potential for government action will always be a risk for this small-cap company.

As with all smaller companies, they can come with risks, as they often require growth to continue and scale.

It’s important as ever to do your due diligence and stay aware of changing situations. This story offers plenty of growth, and it continues to ride the coattails of AI investment. If it can show signs of scale as sites are added, we could see continued success.

Acusensus: The AI highway cop

An AI highway cop sounds way more intimidating than a parking inspector.

Arnie running Terminator-style down the highway to halt speeding drivers. It’s not quite that, but Acusensus has developed AI-enabled enforcement systems. The hardware and software detect drivers engaging in illegal activity, including mobile phone use while driving, speeding and seatbelt compliance.

The company’s flagship product is the Heads-Up solution. It’s fixed or trailer cameras capture high-resolution images, AI detects whether an infringement occurs.

Acusensus’ Harmony product provides fixed, trailer and in-car speed enforcement with all-weather imaging.

The technology drives behavioural change. Non-compliance drops when drivers know cameras can see them.

Acusensus listed in 2023 and has a current market cap of around $250 million.

After launching a world-first enforcement program in NSW back in 2020, Acusensus expanded through Australian state government contracts and is now pushing into overseas markets. This includes deployments in New Zealand, the UK, and the United States, tapping into huge global markets that Acusensus needs to continue to grow. When you factor in fixed hardware (in some cases), AI software and high-quality outcomes, the products contracts and integrations create stickiness.

Great growth, but a little pricey?

Acusensus has strong revenue growth, compounding at 27.5%, but ultimately has yet to make a profit.

Authorities issue and collect the fines. Unlike Smart Parking, Acusensus doesn’t collect the fines issued, and earns fees for its systems and services. The government pays Acusensus regardless of how the public behaves.

This could still be a while off, too, which adds to the risk of holding the company. What if it can never generate profit? Trading on a 2025 revenue multiple of ~4x, it is pricey for a company with a 45% gross margin. It does have sticky multi-year government contracts in its favour. With signs once they’re in with a state, they can add additional services on top.

Investing isn’t risk free, and Acusensus is no exception.

Adding to the risk is the overhang of legal issues. Back in June this year, Acusensus announced that Redflex Traffic Systems began legal proceedings against the company. Redflex is alleging ownership of certain Acusensus intellectual property, including patents, stemming from matters about eight years ago. Acusensus notes that it disclosed a competitor’s IP allegations in its 6 December 2022 IPO prospectus and says it will vigorously defend the claims

While these risks aren’t exclusive to small capitalised companies, they are part and parcel of investing.

One to add to the watchlist.

The takeaway for Raskals

Beyond AI, private parking standards are tightening, regulators are pushing out rogue players and encouraging more technology. Road safety continues to be prioritised with governments under pressure to improve road safety, while AI and automation create a financially viable end product.

So while neither has been built by AI royalty, both are targeting changes in vehicle behaviour.

Both these have the potential to grow from the small market caps they are today into much larger companies, they do carry risk. So small, in fact, that neither are available in the ATEC ETF. If you were wanting to hold personally for your satellite portfolio, I’d recommend digging further and building out your thesis before creating a small position.