Commonwealth Bank of Australia (ASX: CBA) and National Australia Bank Ltd. (ASX: NAB) shareholders are wondering how their bank shares will be affected by the current sell-off and market squeeze.

I received quite a few emails from our Rask Invest members asking how low-interest rates and the economic downturn will affect bank profitability, as well as insurers such as Insurance Australia Group (ASX: IAG) and Suncorp Group (ASX: SUN).

Take it from me, the short answer is no analyst can tell you exactly what comes next for the Australian banks, but there are a few things that I believe are now more likely than ever.

Dividends will be cut. Hard.

Dividends will be cut, for a multitude of reasons. The historical dividend yields for CBA and NAB shares currently displayed in your brokerage account is a mirage. With some banks offering up to six months of no repayments to mortgage holders, the cash flow will dry up very quickly.

Admittedly, the banks will try and get what they can from the Government coffers during a downturn, as they did during the GFC.

However, if you ask me, the banks have been wanting to cut dividends for years, so they can retain more of their capital to fund their future growth plans. So depending on how you look at it, cutting dividends now might actually be a good thing for the banks in the long run.

Bad debts will spike.

Despite Government stimulus and the banks’ best efforts, thousands of Australian households will go overdue or default on their loans. Bad debts across all Australian banks, including Westpac Banking Corp

(ASX: WBC) and ANZ Banking Group (ASX: ANZ), have fallen to near-record lows in recent years. It’ll be a long time — perhaps never — before we see that again

From an accounting perspective, when a bank incurs bad debts they are taken straight from the income statement. Meaning, they directly cut into reported profit. As you can imagine, this deduction loops back into dividend payments, since many of Australia’s banks pay dividends based on the percentage of their reported profit.

Rising bad debts and high unemployment numbers are a medium term (2-3 years) to long run (5+ years) consequence for the banks and their shareholders. Although it’s somewhat different this time around, long-running NAB shareholders will remember that it took the bank well over five years to rid itself of the bad loans incurred during the GFC. That’s why NAB severely underperformed other banks.

Lower profits, for longer.

In a low-interest-rate environment, Australia’s banks have found it very hard to maintain their profitability. You can see this in the net interest margins or NIMs. Now with even lower rates, I wouldn’t be surprised to see lending margins stay below 2% for a very long time.

Outside of lending, there is little reprieve. Following the banking Royal Commission, Australia’s banks no longer have their financial advice and funds management businesses to deflect some of the pain in lending.

Hybrids will convert.

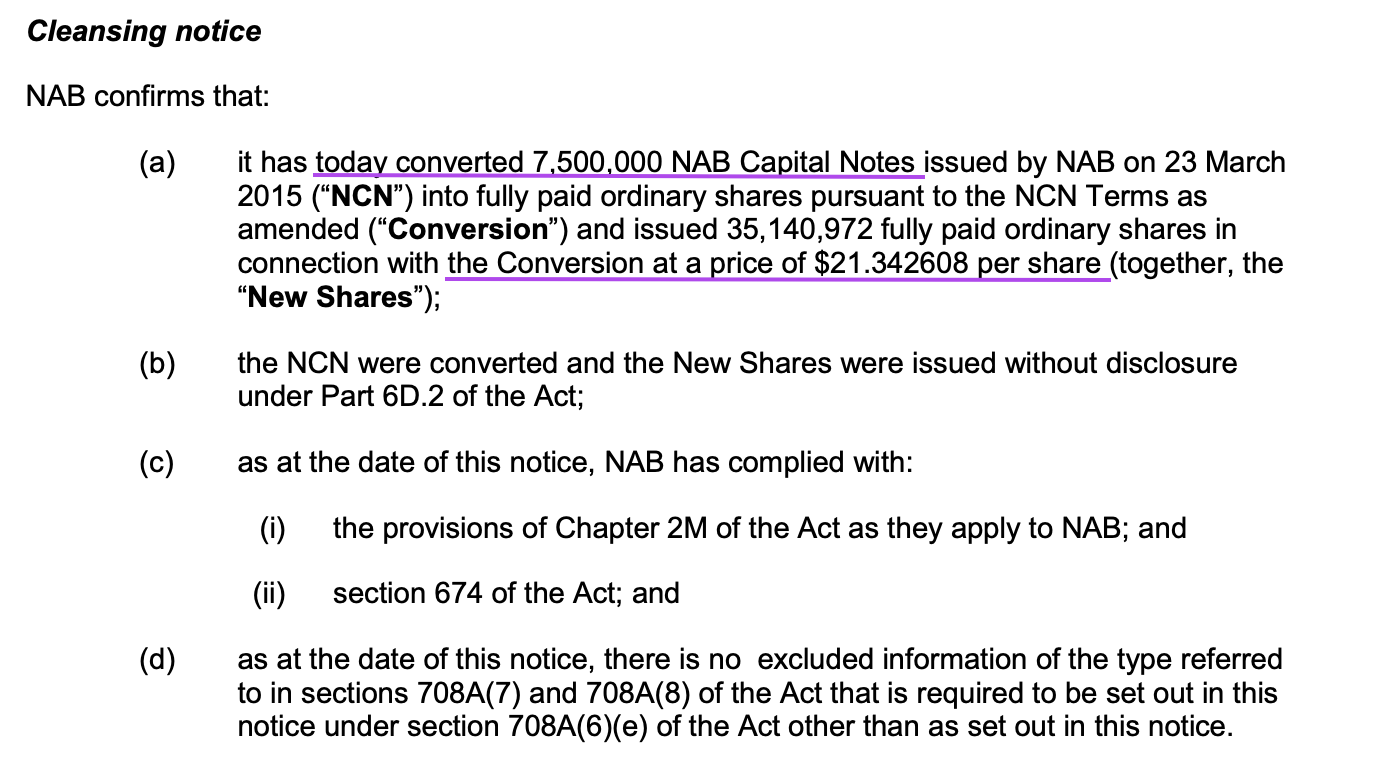

According to NAB’s update today, the bank has already started converting certain hybrid investments into ordinary shares:

Investors who had purchased these hybrids on the assumption (or advice!) that they were safer than normal shares are now feeling the pinch of being sold into a product that was too complex for normal investors to understand.

The conversion means existing shareholders are diluted (because there are more shares available). Also, it will likely put further pressure on the share price in the short term. And the investors are no longer likely to receive the same level of dividend repayments as they would have with a hybrid.

Buy, Hold or Sell

I don’t believe Australia’s bank will go bust in the current market crash, and the likely credit squeeze we’re about to experience.

Australia would throw everything at the banks before they let one of them fail. However, please note that even if the Government did bail them out they would want their pound of flesh in the form of equity or debt.

The bottom line for shareholders is that I do not believe it’s worth owning CBA and NAB shares for dividends. I’d consider buying at much lower prices and probably in 6 months from today, once the dust has settled. The near-term uncertainty and questions over their long-term profitability concern me.

However, I would consider owning a low-cost and diversified dividend ETF or a simple market cap ETF. At least with a diverisifed ETF you won’t be dependent on fully franked dividend income from just one sector: banking.

If you have capital gains tax liabilities built up from owning bank stocks for many years you wouldn’t necessarily have to sell out all at once. You might simply reinvest your dividends or capital back into an ETF over time.

Our Rask ETF strategy includes our #1 dividend pick.

[ls_content_block id=”18457″ para=”paragraphs”]

Disclosure: Owen does not own a financial interest in any of the companies mentioned.