Higher rates can help banks, until bad debts start catching up.

ASX bank shares are an Aussie favourite.

The consistent dividends feed franking-credit-hungry investors, while structural government support for housing and an oligopolistic market structure support significant barriers to entry.

But with two recent rate rises from the RBA and uncertainty around further movements, what does it mean for the banks?

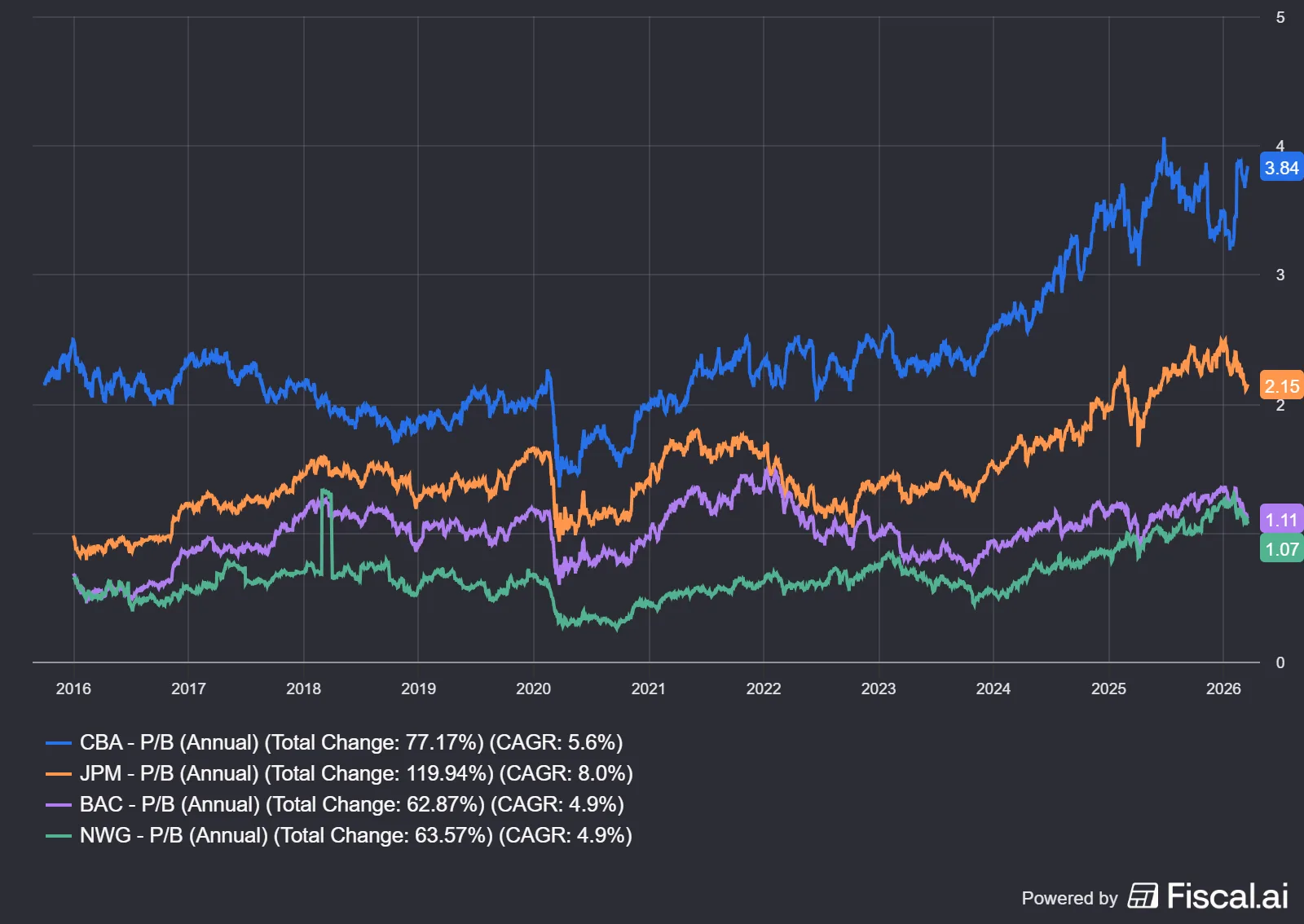

Investors often look at price-to-book value which gives a quick sense of what the market is paying for a bank’s balance sheet. That matters more for banks than it does for most other companies. A bank’s value comes down to the quality of its loans, the strength of its capital base and its ability to earn solid returns without taking silly risks. Australian banks also tend to trade at higher price-to-book multiples than many banks overseas. Part of that comes back to structure; a handful of major players dominate the Australian market.

Commonwealth Bank of Australia (ASX: CBA) is the obvious example. Investors have often been willing to pay a premium for the bank compared to overseas peers. Investors appear to view it as a high-quality, lower-risk bank.

Market structure has also helped support that premium, with passive fund flows and Commonwealth Bank’s large index weighting underpinning demand for the shares.

So, how does a rising interest rate environment impact the banks?

Higher interest rates and the impact on bank profits

Higher interest rates can boost bank profitability because banks earn a spread (net interest margin) between what they pay on deposits and what they charge on loans.

Net interest margins often expand when rates rise quickly, lifting earnings and dividends. Yet rising rates also mean borrowers face higher repayments, which increases the risk of defaults and bad debts. If unemployment rises or house prices fall, banks may need to set aside more provisions for loan losses. Raskals, therefore, need to look beyond simple ratios and consider the broader economic context, regulatory environment and the bank’s balance‑sheet strength.

Banks with conservative lending standards and strong capital buffers can navigate an uncertain cycle more effectively.

The impact of the regulator on bank profits

Regulation is another important factor.

Australian banks operate under the watchful eyes of the Australian Prudential Regulation Authority (APRA) and ASIC. Capital requirements ensure banks hold sufficient equity to absorb losses, while responsible lending rules limit excessive risk‑taking. Tight regulation has historically helped Australian banks weather global crises relatively well, but it can also constrain growth. When rates rise, regulators may stress-test banks to assess their resilience to economic downturns. Understanding each bank’s exposure to different loan types (mortgages, business loans, credit cards) helps gauge how rising rates might affect profitability and defaults.

For instance, banks with a high proportion of fixed‑rate mortgages may see slower margin expansion compared to those with variable‑rate loans, but they also face lower default risk if rates spike.

The Rask recap

Bank stocks can still be attractive in a rising interest-rate environment, but they are not automatic buys just because rates are going up.

Higher rates can support margins and earnings. The trade-off is that they also put more pressure on borrowers and can lead to higher bad debts. Investors must focus on the quality of the loan book, capital strength and whether the bank is being paid enough for the risks it is taking.

The best opportunities are usually the banks that can grow earnings without stretching credit quality, even if that means paying a little more for quality.