Earnings season was brutal. At the smaller end of the market, three ASX small cap winners stood out, delivering encouraging numbers.

Reporting season volatility ramped up again in February.

Volatility, though, for the smaller end of the market is a well-worn path. With thin liquidity and less analyst coverage, the market can re-rate or de-rate a company in one session, regardless of the underlying result. In a market with inflation anxiety, monitoring CPI or interest-rate chatter makes small caps vulnerable. Often considered higher risk, when rates are rising, investors seek larger, “safer” assets (you know, like CSL – down ~20% since reporting). Wading through the volatility, ultimately, these are businesses, albeit smaller than your usual headline grabbers, and they are performing. We take a look at 3 ASX small cap winners that may be worth digging further into.

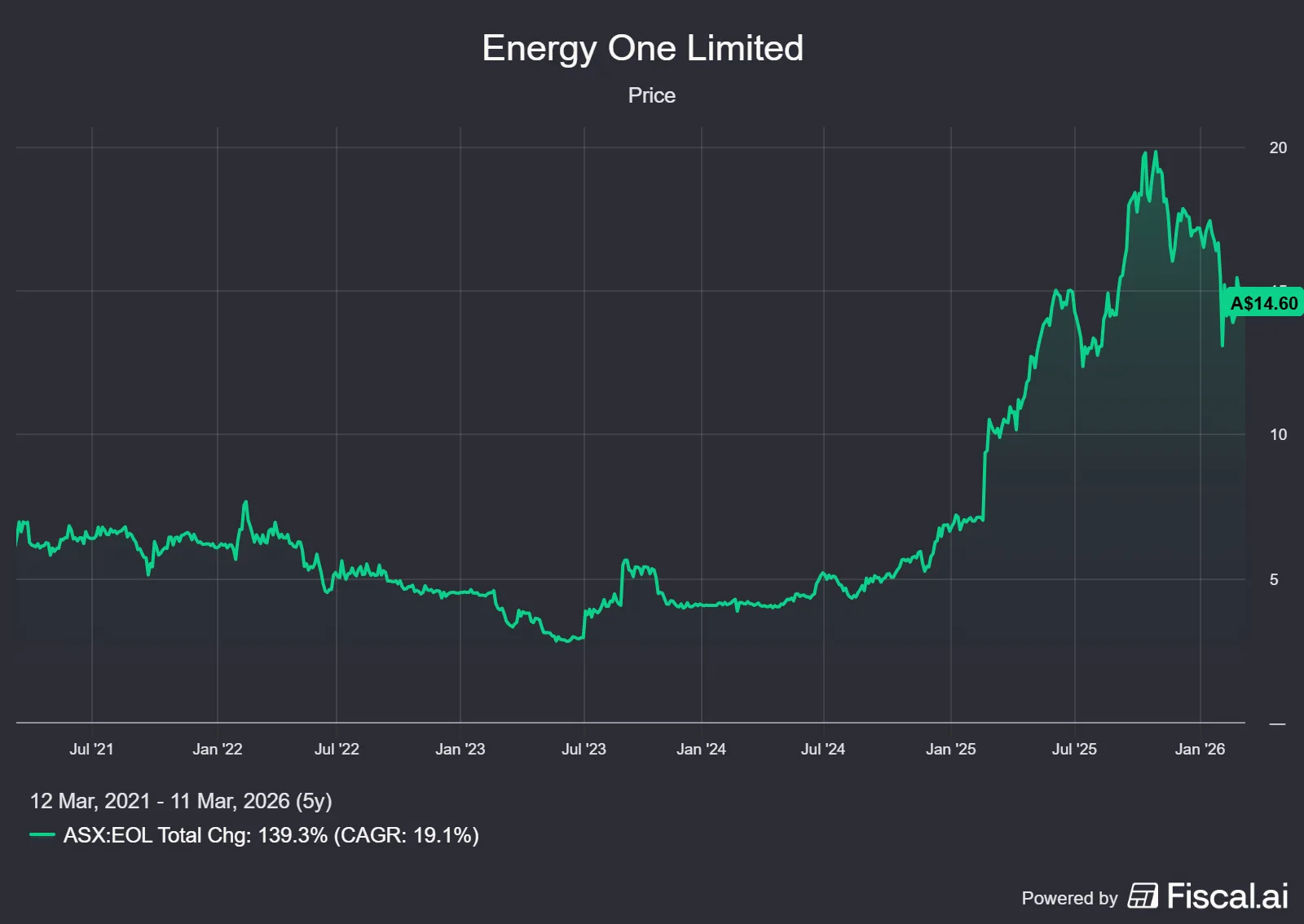

Energy One’s recurring revenue and operating leverage

Energy One Ltd’s (ASX: EOL) half-year report produced a strong result.

We’ve previously written about Energy One here.

Energy One reported revenue of $34.8 million (+21%) and profit after tax of $4.0 million (+61%), showing tremendous scale. The business is now generating 90%+ recurring revenue.

The market craves recurring revenue and the perceived certainty that it brings. Energy One sits in the heart of the small-to-mid cap band at roughly $450m market cap, making it small enough to really move up in market cap, and big enough to matter to funds.

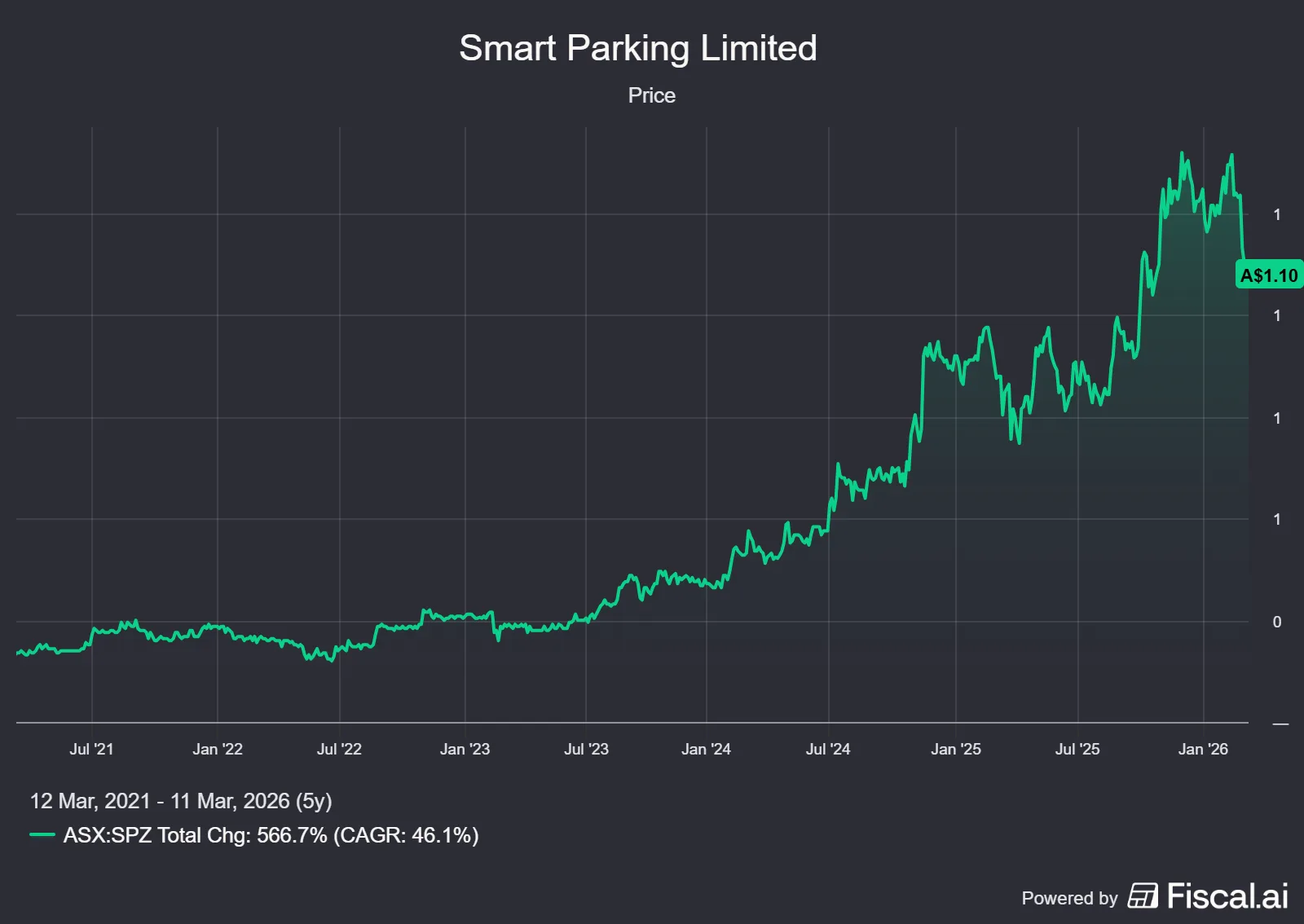

Smart Parking scale shows up in the P&L

Smart Parking (ASX: SPZ) has been building a larger, more global platform for a number of years now.

The $445 million market cap listed parking inspector collects Parking Breach Notices (PBN’s) using its camera technology for private parking bays. Its first half of 2026 results showed continued growth. More sites and the US acquisition lifted revenue to $62.6m (+96%) and adjusted EBITDA of $15.6m (+85%).

It is worth noting the flat growth in PBN’s in the UK. Smart Parking cited cost of living pressures, but something to watch going forward to make sure it’s a one-off and not a pattern.

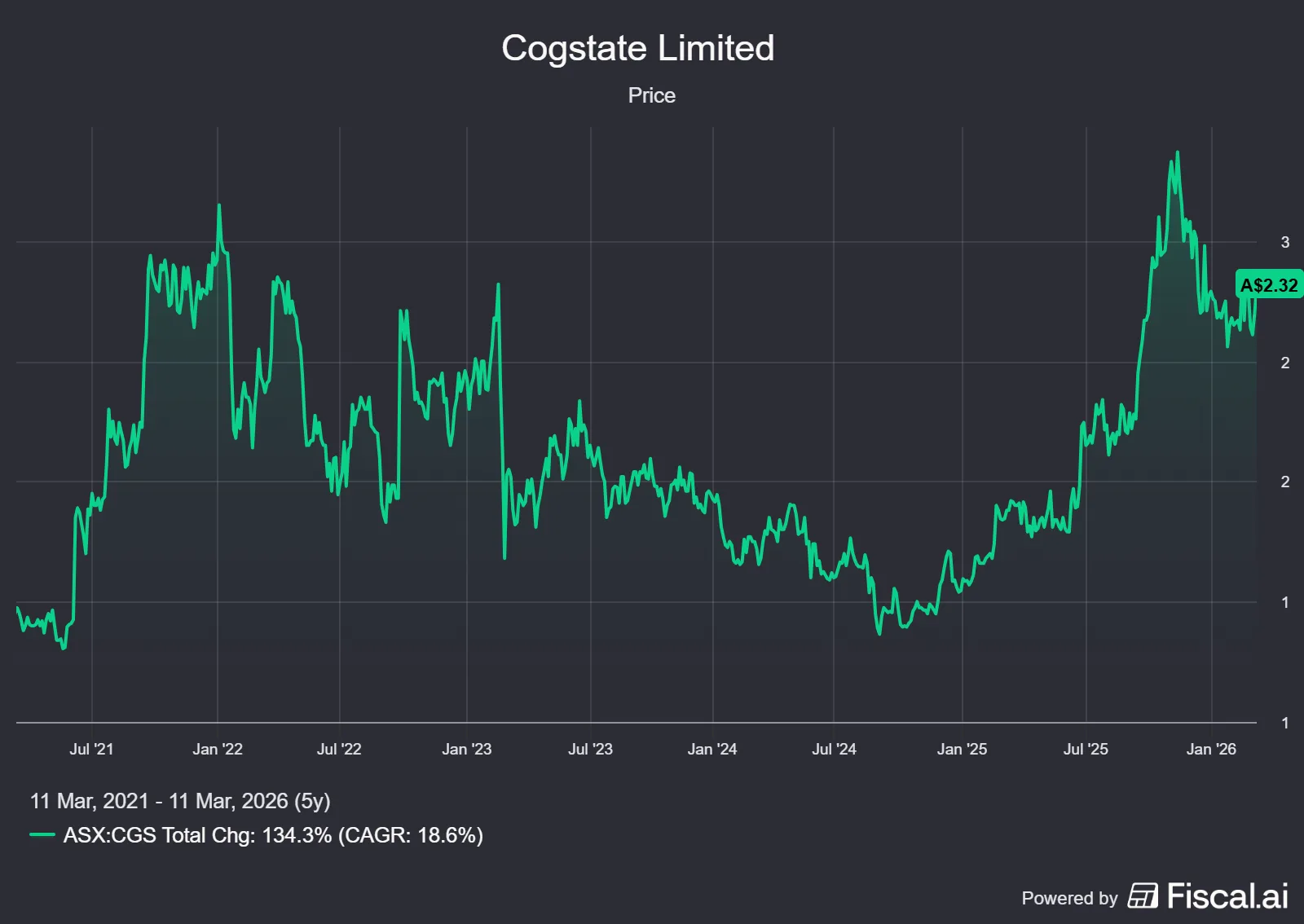

Demand grows for Cogstate

Cogstate Ltd (ASX: CGS) partners with drug developers to help measure clinical trial endpoint data for accuracy, with a focus on the central nervous system.

Revenue increasing to $26.9 million (+12%) while operating expenses fell 9%, which is exactly what you want to see as the business scales and costs drop as a percentage of revenue. The only “messy” bit was gross margin down to 52.8% from 61.4% last year. Management says the margin dip is temporary, a trade-off to win market share, with a rebound targeted to 56–59% in the second half and 60%+ longer term.

At a market cap of $400 million, Cogstate deserves a spot on your small-midcap watchlist.

The final word

With each earnings season that goes by, reactions to results feel more volatile than ever.

For small caps, every 6 months, you get a clearer picture of how the company is performing. Each of the above companies shone in different ways, but all grew revenues and profits by even more, delivering on scale, which investors crave. whether the company is growing.

In a volatile reporting period, that combination is often what separates a good result from a company that investors are willing to pay more for.