Data#3 (ASX: DTL) H1 FY26 results delivered record gross sales, but Microsoft incentive changes squeezed margins and profit.

Unfortunately, this earnings season, steady results aren’t enough for the market.

Data#3 half-year results couldn’t stop investors from selling on Monday. Record gross sales and tight cost control were offset by software solutions margin pressures as Microsoft incentives changed. Management says the business has moved through the worst of the transition.

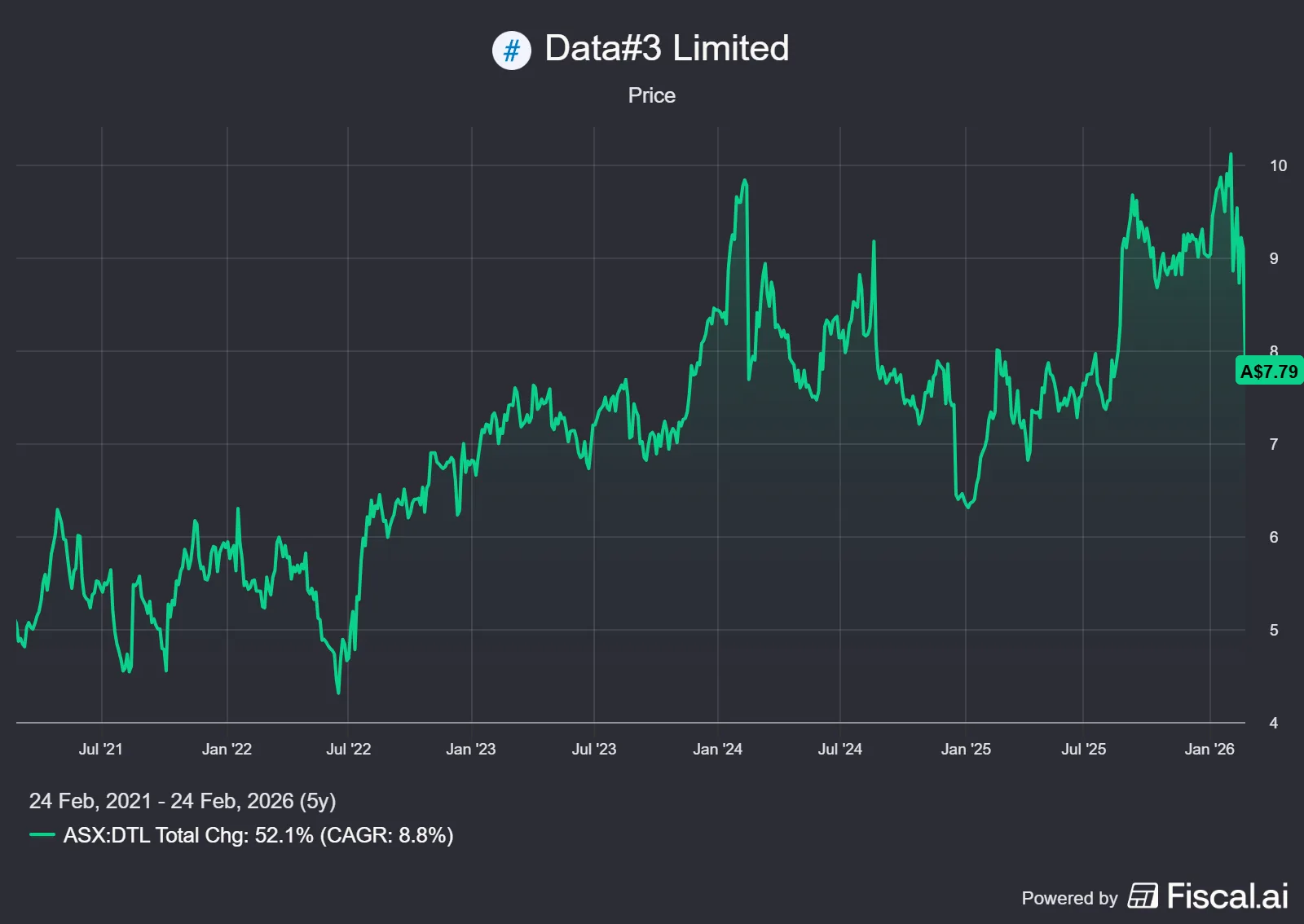

Mr Market took exception, with Data#3 a touch under analyst expectations for operating earnings (EBIT and EBITDA). Shares ended down 14.4% to $7.79 the day of the first-half result.

Key points in Data#3’s half-year results

- Gross sales +9.2% to $1.54 billion; statutory revenue +8.1% to $423.1 million.

- Gross profit +0.3% to $144.0 million, with gross margin down to 9.3% (10.2% pcp), reflecting lower software incentives.

- Net Profit Before Tax +4.5% to $33.5 million, Net Profit After Tax +3.7% to $23.2 million, earnings per share +3.6% to 14.95c.

- Interim dividend 13.50c fully franked (+3.1%), the company paid out ~90% of its profits.

- Balance sheet remains conservative: no borrowings, cash $125.4 million.

- Operationally, Data#3 highlighted ~70% recurring revenue and noted its sales growth outpaced Australian IT market growth cited for the calendar year 2025.

What happened in Data#3’s half-year results?

The half boiled down to mix and margin.

Growth was healthy in infrastructure, software volumes held up, but profitability softened and services were mixed.

The software margin decline is the core concern.

Software gross sales rose ~9%, supported by Azure/Cloud Service Provider (CSP) growth and non-Microsoft vendors. However, Microsoft channel incentive program changes compressed software gross margin (3.5% vs 4.0% last year) and pulled down segment profit. In simple terms, Microsoft changed how it pays partners. Data#3 received less incentive or rebate income per dollar of Microsoft software or cloud sold. Squeezing margins.

Management called out end-user computing growth of over 30% and data centre sales up ~30%. This segment’s operating leverage was a meaningful offset to the weaker software margin.

Services were a tale of two segments.

Managed services and consulting grew (wins and renewals), while customers delayed decisions and reduced contractor usage, keeping project services and people solutions (recruitment and contractors) flat. Management linked project delays to budget uncertainty, higher decision complexity, and more stakeholders involved in procurement.

Management noted on the call that its now 9 to 10 people in an organisation involved in the decision-making process, where it used to be 3 to 4.

What impact does this have on Data#3?

Software is the largest portion of gross sales, so a small move has a huge impact.

Management characterised the December half as the most impacted period by the Microsoft changes. As these changes took effect on 1 January 2025, the incentive reset is largely behind the company and should be immaterial in the second half.

Data#3 is actively moving beyond the change by replacing the incentive dollars with fee dollars.

The company is charging customers directly for the work they already do in software, such as licensing advice and subscription optimisation, to replace the profit lost from lower rebates.

Infrastructure is doing the heavy lifting, but management also flagged potential price increases due to memory constraints and supply constraints. This can pull forward demand (customers buying early) but could also delay deliveries and invoicing late in the year if stock is constrained.

Outlook and guidance for Data#3

Data#3 did not provide formal guidance

The company reiterating seasonality with sales peaking in May/June and earnings weighted to the second half.

However, the earnings call effectively did give investors a framework:

- Management said the prior view of high single-digit FY26 gross profit growth is unchanged, with commentary implying ~7–9% would be a strong outcome given 1H incentive pressure.

- Software is expected to return to gross profit growth in the second half, with full-year software gross profit consistent with FY25. Management is targeting a return to pre-change profit growth trajectory into FY27 (even if revenue grows faster than profit).

- Infrastructure momentum is expected to continue, with the memory theme a potential near-term tailwind but also a possible Q4 headwind due to availability and invoicing timing.

- Management expects low to mid-single-digit service growth, with managed services strength offsetting slower project and contractor markets.

- The company also guided to staff costs up ~2% for FY26 and other operating expenditure up ~5% (ex staff), supported by restructuring benefits, role discipline and automation efficiencies.

Overall Data#3 continues to work through a transition period.

If you were to annualise the earnings per share, even after the drop, Data#3 is trading on a price to earnings ratio of 26, which is a lofty multiple in my opinion if you’re only growing earnings per share at 3.6%.

Data#3 will need hit the growth management alluded to and achieve a much stronger second half to maintain the valuation. Even that might be a stretch.