HUB24 Ltd (ASX: HUB) half-year results show record platform inflows and expanding margins as superannuation switching accelerates growth.

HUB24’s half-year result was strong with signs pointing to further strength beyond the half.

The company posted record platform net inflows of $10.7 billion, lifted group revenue 26% to $245.9 million, and expanded underlying EBITDA margin to 42.7% as the platform scaled.

A reminder, HUB24 is a wealth platform used by financial advisers to run client portfolios. It provides the back-end services, including custody, administration, trading, reporting and super/pension accounts. HUB24 earns fees primarily from funds on the platform (FUA) and from activity-based revenue (cash and trading). It also sells adviser technology tools through its Tech Solutions segment.

It’s the story behind the inflows that inspires. Superannuation member switching is driving more inflows, helped by demographics and retirement-driven advice demand.

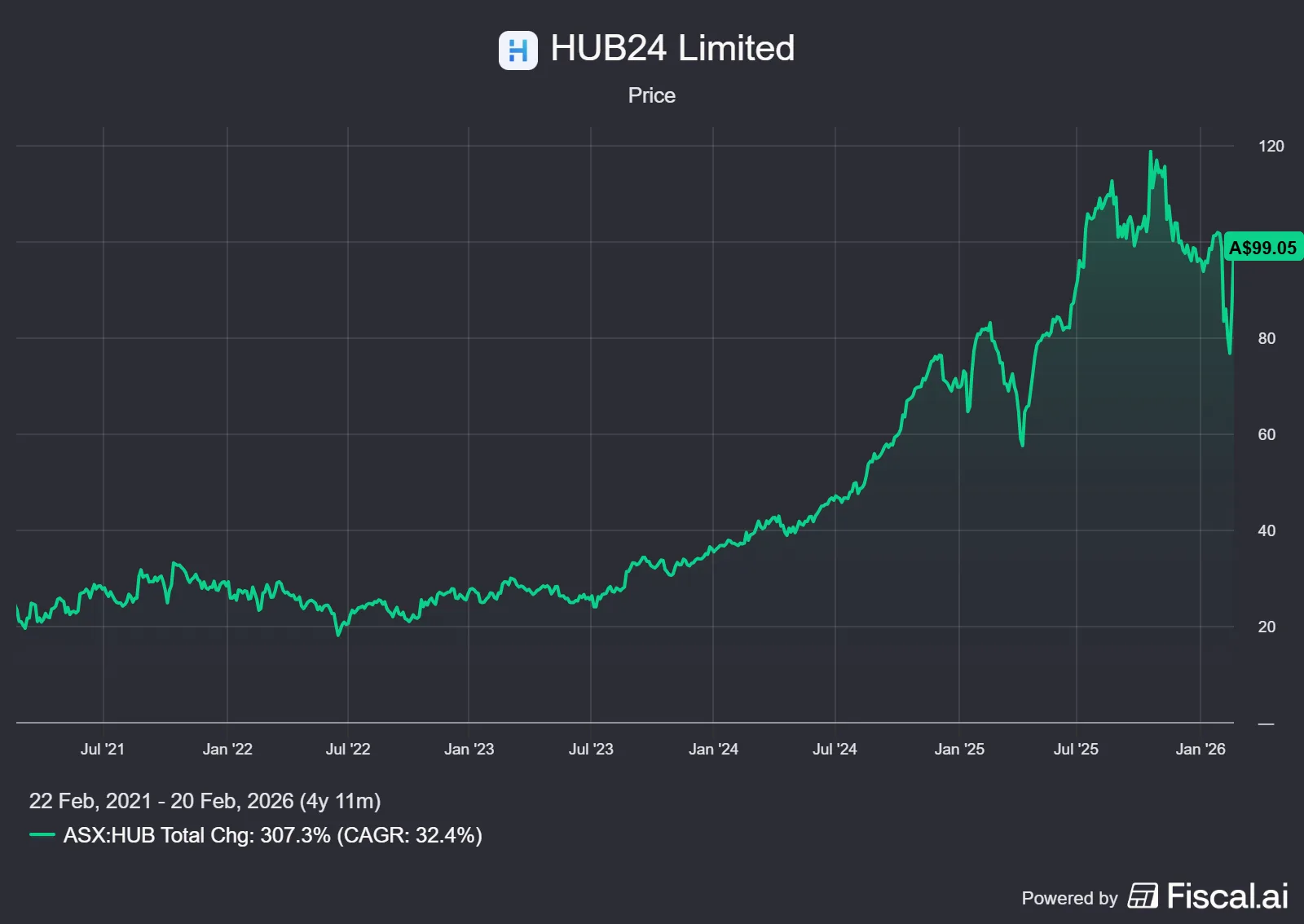

The market loved the HUB24 half year results, with the expectations beat, the HUB24 share price was up 14.16% on the day to $98.45.

Key points from HUB24’s half year results

- Net inflows (Platform): $10.7 billion in the half (+13% YoY). Management described it as a company and industry record, and HUB24 remains the #1 for platform net inflows for eight consecutive quarters, including leading “competitive” switching flows.

- FUA: total $152.3 billion at 31 Dec (Platform $127.9 billion + PARS $24.4 billion). Platform FUA was $129.8 billion by mid-February.

- Financials: revenue $245.9 million (+26%), underlying EBITDA $104.9 million (+35%), margin 42.7% (+290bps); underlying NPAT $68.3m (+60%); statutory NPAT $59.7 million (+80%).

- Strong platform economics: custody revenue margin stable around 32bps, with tier/cap effects offset by cash and trading contribution.

- Dividend: interim 36c fully franked (+50%)

- FY27 target upgraded: Platform FUA target lifted to $160–170 billion (from $148–162 billion).

What happened?

On the call, management noted the underinvestment in the retirement service industry as a real tailwind, this is now showing up in members actively switching away from traditional funds and seeking adviser solutions.

It’s not just switching that is driving growth. HUB24’s existing base is growing. In fact, 92% of flows came from existing advisers, which tends to be stickier if service levels hold. Management also noted advisers are increasingly standardising. Research cited showed 36% of advisers now prefer a single platform, up from 13% in 2021.

HUB24 is growing revenue, but most importantly, it’s scaling. Platform underlying EBITDA margin expanded to 46.7%, showing benefits are still coming through despite ongoing investment. “AI” got a mention 9 times in the transcript (probably low vs a lot of others!) although management emphasised continued investment in new technologies, new productivity, new features and benefits.

HUB24 generated $78 million of operating cash flow (after tax payments). The cash balance did drop, HUB24 noting changes in regulatory requirements and an increase in the super fund’s operational risk reserve requirement.

The outlook for HUB24

It was a very positive result with the market lapping up the result, albeit after it had been sold down.

Looking forward, a very positive upgrade to FY27 platform FUA driven by flows. Management referenced a “base case” of ~5% market growth plus ~$18–20 billion of net flows in FY26 and FY27 to land near the middle of the range, with no large transition assumed in the base case.

HUB24 is riding a genuine retirement-and-advice switching wave, and with platform scale still expanding margins, the future looks bright for HUB24.