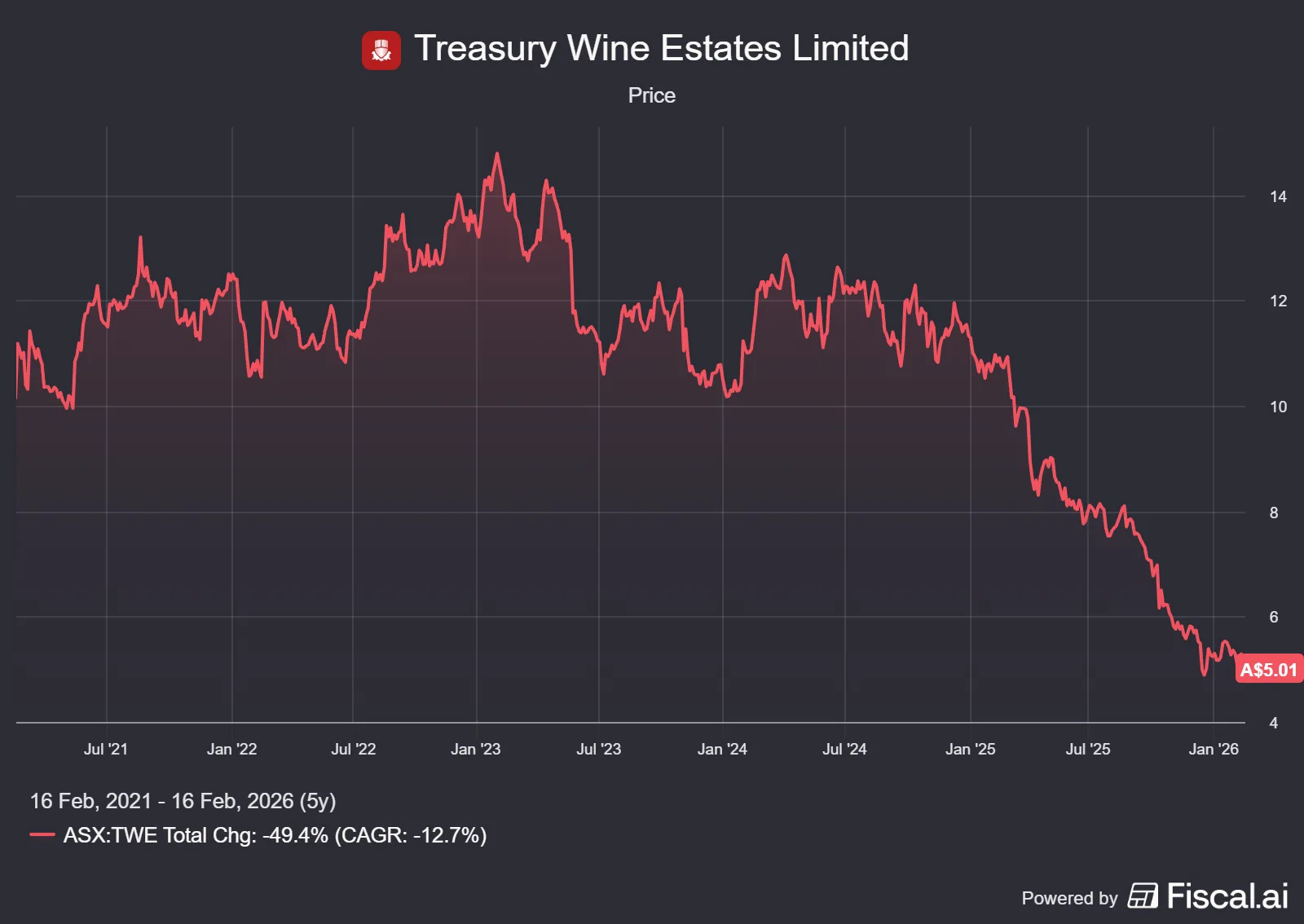

Treasury Wine Estates (ASX: TWE) had already flagged much of its HY26 result, yet shares are still dropping more than 5% and the interim dividend was scrapped.

A quick refresher: Treasury Wine Estates is a world leader in winemaking and brand marketing, with approximately 13,000 hectares of vineyards and around 3,400 employees across 70 countries. Some of the more popular brands include Lindeman’s, Penfolds, Pepperjack, Rosemount, Yellowglen and Wolf Blass.

A large non-cash impairment in the US drove the headline loss. In simple terms, the company reduced the accounting value of some US assets, which hurt profit but did not involve cash leaving the business.

Management is now prioritising channel health, cash flow and leverage reduction, meaning it wants to clean up excess inventory in the supply chain, generate stronger cash, and reduce debt, even if that comes at the expense of the interim dividend.

After Treasury Wine Estates closing above its lows yesterday, the share price has dropped a further 5% today as investors drink in the result.

Treasury Wine Estates HY26 results key points

Here are the key points from Treasury Wine Estates’ HY26 result:

- Net sales revenue (NSR) of $1,297.7 million fell 16.0% (-16.6% constant currency), driven by lower shipments across all divisions.

- EBITS (earnings before interest and tax, excluding significant one-off items) was $236.4m (-39.6%). This is a measure of operating profit before financing costs and tax. The result was marginally ahead of the $236 million that had been upgraded from $225–235m last week.

- EBITS margin dropped to 18.2%, meaning the company kept just 18.2 cents in operating profit for every dollar of sales, down from last year.

- Statutory NPAT was a loss of $649.4m, driven by post-tax material items of $751.0m, primarily an impairment of US-based assets.

- Underlying NPAT was $128.5m (-46.3%) and underlying EPS was 15.9c (-46.2%). This strips out one-off items to show the underlying business performance. Even on that basis, earnings were materially weaker.

- Cash of $216 million and debt of $2.1 billion.

- Operating cash flow was $116.2m (down from $259.6m), with cash conversion of 82.4%. Cash conversion measures how much accounting profit turns into real cash, and this remains reasonably solid despite lower earnings.

- Outlook: management expects a stronger 2H26 (California stabilisation post transition) and reiterated TWE Ascent targeting $100m p.a. cost improvement over 2–3 years, with more detail at an Investor Day (4 Jun 2026).

What happened

Management deliberately restricted shipments, meaning it sent less wine to distributors and retailers. That reduced net sales revenue in the short term, but also helped lower excess inventory sitting in customer warehouses.

Short-term pain with the aim of long-term gain. Shipping less now hurts revenue, but should restore healthier ordering patterns and avoid clearance sales, thereby protecting pricing and margins going forward.

You can see the pain across each division:

- Penfolds: NSR $501.3m (-10.1%) and EBITS $201.0m (-19.6%).

- Treasury Americas: NSR $283.0m (-28.4%) and EBITS $44.0m (-63.6%). Softer US market conditions and disruption from the California distribution transition hit shipments and margins.

- Treasury Collective: NSR $513.4m (-13.2%) and EBITS $28.1m (-51.1%). The US was weak, but Australia showed better momentum in premium brands.

The issues didn’t end there

The statutory net profit was dominated by the non-cash impairment of the US assets. A severe goodwill writdown of selected assets and write-down of excess bulk wine.

Further distribution headaches during the RNDC-to-Breakthru changeover in California impacted shipments. Management highlighted stabilising trends in January and expects that this will continue in the second half.

Penfolds sales in China improved, but TWE still kept shipments tight because too much wine was leaking into grey-market channels and being sold at discount prices. By limiting supply, they’re trying to protect premium pricing and rebuild control over the distribution network.

The interim dividend was suspended to preserve cash and begin balance sheet repair. With cash of $216 million and debt of $2.1 billion, management clearly sees the need to strengthen the balance sheet before restoring shareholder payouts

A challenging result to say the least. It shows the enormity of the task ahead for recent CEO hire Sam Fischer.

What it means and the outlook

Treasury Wine Estates expects 2H26 EBITS to be higher than 1H26, reflecting an improving second half, particularly California.

Management pointed to divisional earnings trajectories of ~$400m FY26 EBITS for Penfolds (around a 40% margin) and ~$90m FY26 EBITS for Treasury Americas (excluding any net benefit from the RNDC settlement). The group continues to run a two-year channel inventory reduction program, which will keep shipments disciplined in the near term, while TWE Ascent targets ~$100m per annum in cost improvement over 2–3 years, with initial benefits expected from FY27, with more detail at the June 2026 Investor Day.

Treasury Wine Estates is obviously in a transition period.

The declining tailwinds of alcohol consumption have me sitting on the sidelines watching. If you’re considering a position, we may be at rock bottom, and these changes could be the turning point. That is what you would be clinging to.

I’ll wait for the execution to become clearer.