ASX tech was one of 2025’s worst places to hide. The question for 2026: is this a blip, or the start of a longer reset?

WiseTech, Xero and NextDC didn’t lose their moats overnight. Leverage, pricing changes and “swing for the fences” M&A forced the market to reprice risk.

For every news headline about AI bubbles and the Magnificent Seven taking over the S&P 500, ironically, the ASX technology index was punished. With a 21% drop in the Technology index, it was one of the worst places to hide on the ASX in 2025. The nuance of the ASX is a little misleading. Given the size of the top ASX technology companies, any negative movement in these giants can have an outsized influence on the total index. So while the top end was in the red, there’s still some life under the hood.

While it’s easy to throw the baby out with the bathwater, long-term investors can still find potential beyond the disappointing 2025.

ASX technology: sector on sale

ASX technology has worn the classic hangover from high expectations and lofty multiples.

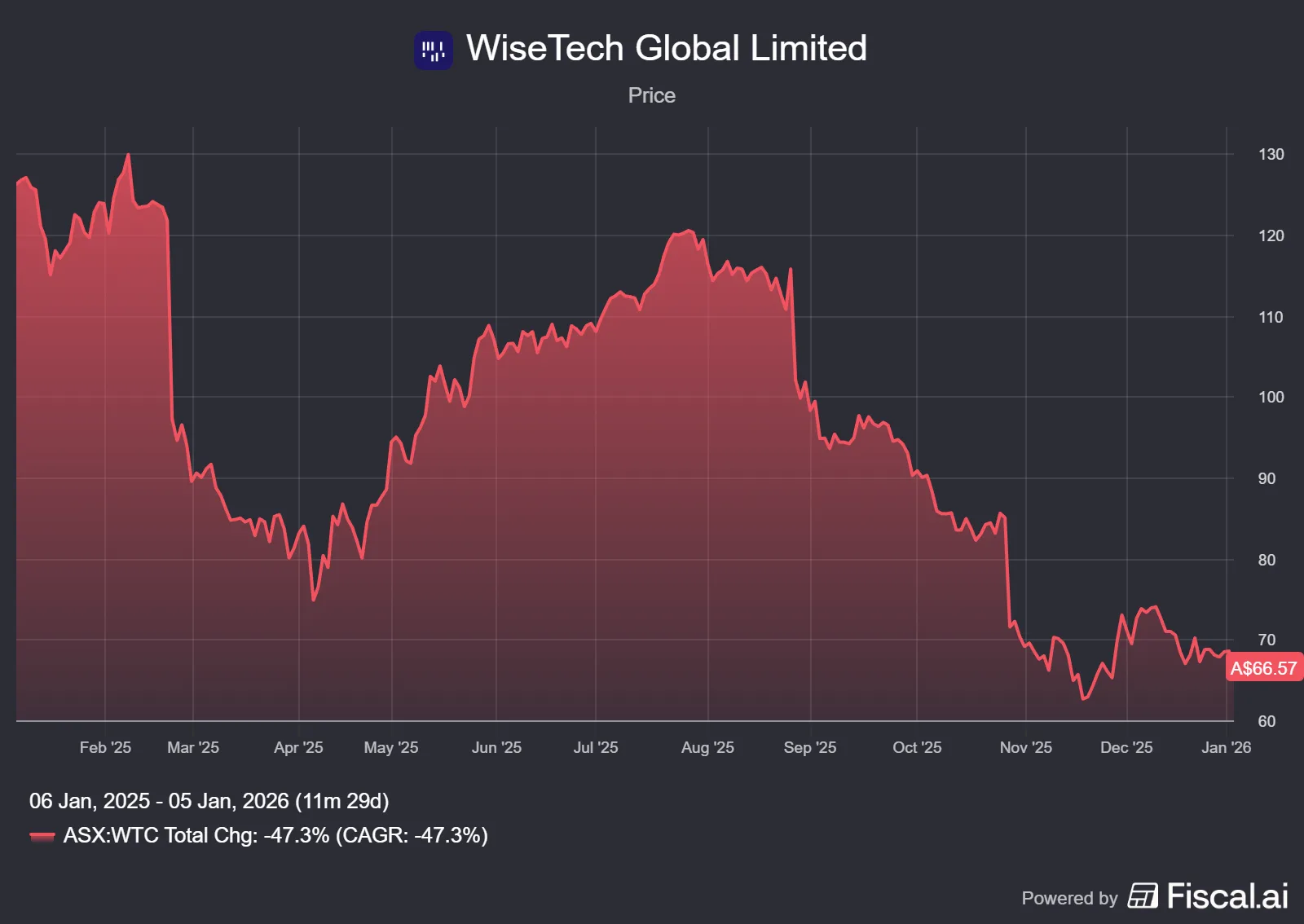

WiseTech Global Ltd (ASX: WTC) is a good example.

Operationally, the business remains a dominant global provider of logistics execution software. Over 16,500 logistics companies use CargoWise across 195 countries, including 46 of the top 50 third-party logistics providers and 24 of the 25 largest global freight forwarders. The thesis of riding the software coattails of this trillion dollar business remains intact.

So why the sell-off?

First, deal risk. WiseTech has just closed its largest acquisition by far, a US$2.1 billion (~AU$3.2bn) purchase of US-based supply chain software group e2open. WiseTech funded the deal with debt, having to now service a new liability and the integration of a new business can make investors a little uneasy.

Second, pricing risk.

A new pricing model unveiled at its 2025 investor day raised concerns and prompted customer pushback. Management argues it better aligns value with usage. Add to that a messy year of very public governance headlines, and it’s easy to see why the market has put this one in the too hard basket.

Additionally, WiseTech founder Richard White experienced significant leadership and legal issues, significantly contributing to a nearly 45% drop in the company’s share price. This included board resignations over White’s personal conduct, federal raids investigating alleged insider trading, and shareholder backlash at the annual meeting. Despite being cleared of misusing company funds, concerns about governance and an ongoing ASIC investigation continue to impact the stock.

In my opinion, these are short term issues, resolved one way or another. If they can fall in the favour of the WiseTech business, I feel this could be a real opportunity with sentiment in the bin and share price hovering in the $60’s.

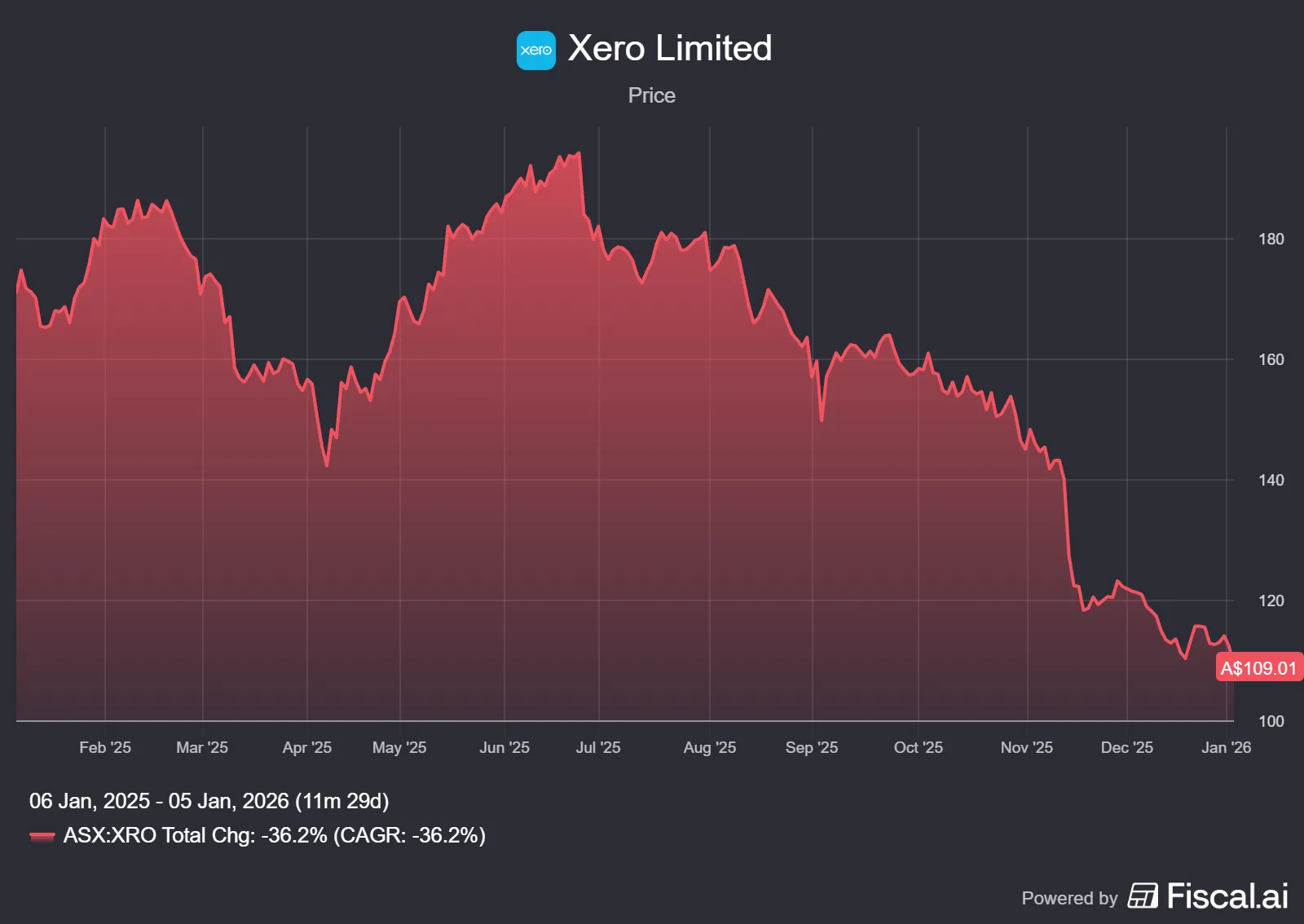

Xero Limited (ASX: XRO) tells a similar story.

The company grew FY25 revenue by 23% to $2 billion, expanding gross profit and the average amount it collects per user, aka Average Revenue Per User (ARPU). Xero’s core moat of deeply embedded cloud accounting software with high recurring revenue, rising ARPU and attractive unit economics is as strong as ever.

Like WiseTech, investors sold Xero shares down sharply in 2025 as they digested the US$2.5 billion (~AU$4 billion) acquisition of US bill-pay platform Melio. Xero funded the purchase with a significant capital raise from shareholders and cash. The deal pushes Xero harder into the US, with the potential to materially lift its revenue mix and ARPU. Xero is paying up a lot for the loss making Melio, with the idea it will bring in a greater share of US customers. There is huge execution risk here given the price paid and the gorilla of a competitor, Intuit Inc (NASDAQ: INTU) who is well established.

In the short term, this kind of “swing for the fences” acquisition is exactly the sort of move that prompts investors to question what they’re willing to pay for Xero. In my view, it’s worth sitting on the sidelines for now and seeing some proof in the Melio pudding.

Then there’s NextDC Ltd (ASX: NXT), despite data centres being a core component of the AI revolution, it’s down in 2025. With the incredible AI capex a significant sector tailwind, and increasing utilisation, NextDC has struggled.

The problem is the P&L and balance sheet timing. FY25 revenue grew, but losses grew faster NextDC absorbed higher staff, power, maintenance and property costs and locked in a new $2.9 billion debt facility to fund the next leg of capex. For investors now more sensitive to leverage and negative free cash flow, the “build it now, harvest it later” model has become harder to stomach, even if the structural AI demand case remains strong. I’m more interested in capital light, AI exposure, with less reliance on debt.

Was 2025 a blip? Or more pain to come?

So, where does that leave investors looking ahead of 2026?

At the sector level, Information Technology could easily remain volatile. The threat of higher interest rates can place pressure on valuations. Investors often see technology and growth as higher risk, so when fixed interest (like term deposits) offer higher returns, investors can seek these out at the expense of growthy tech.

It can also create a rotation into what is perceived safer or “boring” cash-generative value names. Any earnings or integration disappointments will keep pressure on what could still be considered high multiples.

My final thoughts

Stepping back from the noise, in my view, WiseTech is the most appealing prospect of the three. WiseTech sits at the heart of global trade flows, while the business is continuing to grow earnings per share. If it can work through the current issues, I believe there is a re-rate around the corner.

Xero still controls a sticky, growing global small-business accounting platform with rising ARR and a potential for a long runway in North America. The question is whether it can eat into that US pie and take some of Intuit’s share. NextDC owns scarce, power-dense data centre sites leveraged to the AI capital expenditure cycle, can we start to see some further signs of scale?

The market has spent 2025 repricing the risk side of the quality-growth equation. For patient investors willing to look long term, that repricing may well set up the next phase of returns. The challenge in 2026 won’t be finding growth, it will be distinguishing between those former market darlings that can execute through this reset, and those for whom the derating is telling you something more.