Pro Medicus Limited (ASX: PME) may be the best operating company on the ASX.

I do not say that lightly. But I am very biased – I bought shares in 2017 and still own some today.

Plenty of companies grow quickly but burn cash.

Others produce lovely margins until competition arrives.

Some have aligned founders but carry enough debt to make a banker sweat.

Pro Medicus has rapid organic growth, enormous margins, recurring revenue, major paying customers, strong cash conversion, founder ownership and no debt.

That is a rare collection.

The Pro Medicus share price is a different question.

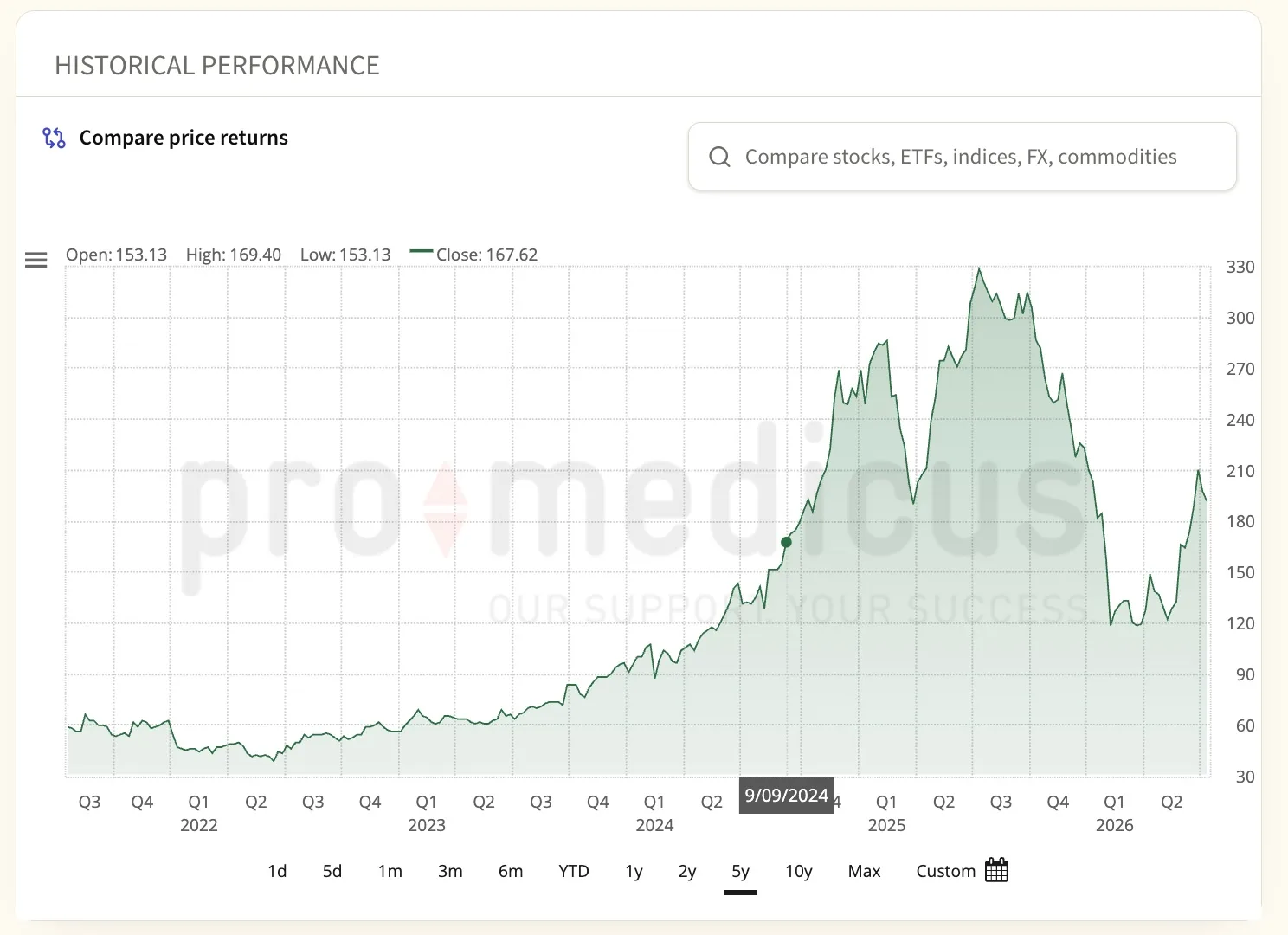

PME closed at $192.62 yesterday. That was about 42% below its 52-week high of $330.48, but still valued the company at roughly $20 billion using its latest reported share count.

Cheaper than before?

Absolutely.

Cheap?

Steady on.

I think Pro Medicus is an exceptional business. I also think investors buying today still need an exceptional future.

Those statements can both be true.

What does Pro Medicus actually do?

Pro Medicus sells medical-imaging software.

Technically correct. Practically useless.

Here is what the product actually does.

A patient has a CT scan, MRI, mammogram or other imaging study. That examination may contain hundreds or thousands of images. A radiologist needs to open the study, retrieve previous scans, compare changes, manipulate three-dimensional views, make measurements, check the clinical history and produce a report.

The files can be enormous.

They may sit across several hospitals, outpatient clinics and cloud environments. The radiologist may be working at another site or from home. An urgent stroke or trauma study may need to jump ahead of routine work.

Pro Medicus’ main platform, Visage 7, handles three important parts of that process.

The Viewer is the clinical screen used to inspect and manipulate images.

Workflow routes each study to the appropriate radiologist, based on factors such as urgency, speciality and location.

Open Archive stores and retrieves the imaging data across the healthcare organisation.

Increasingly, customers buy the three products together. Pro Medicus calls that “full stack”.

It is also expanding the same core platform into cardiology and digital pathology.

The older Visage RIS product handles administrative tasks such as scheduling, billing and practice management, mainly in Australia and Canada. It remains a good business, but Visage 7 in North America is the engine.

In H1 FY26, Pro Medicus generated $116.5 million from PACS and Visage products, compared with $8.2 million from RIS. North America contributed roughly 90% of group customer revenue.

Why does Visage matter to a hospital?

A medical image is not especially helpful while it is loading.

Pro Medicus says its advantage begins with proprietary streaming technology. Instead of downloading an entire study to a local workstation before the radiologist can manipulate it, Visage processes the data centrally and streams what the user needs.

That should matter more as imaging files become larger.

Photon-counting CT, cardiac imaging and digital pathology can produce huge data sets. Remote reporting has also become common, meaning the radiologist may not be sitting beside an expensive workstation on a perfect hospital network.

Management claims Visage can display even very large studies in under two seconds and, in most cases, under one second.

It also says customers can achieve radiologist-productivity improvements of more than 25%, sometimes considerably more.

I would not accept those figures as universal fact.

They are management claims. Pro Medicus does not publish a neat customer-by-customer table showing productivity before and after implementation, total implementation cost, outage statistics and performance against each named competitor.

The commercial evidence is still impressive.

Major healthcare institutions keep selecting the product. Management reported that Pro Medicus served 11 of the top 20 US hospitals ranked by US News at the end of FY25. The company also continues to win renewals that add products and increase transaction prices.

That tells me customers see real value.

Nobody enjoys paying more for hospital software.

They especially do not enjoy paying more for another five or seven years unless the product is doing something useful.

How Pro Medicus makes money

Pro Medicus’ North American business generally uses long-term transaction contracts.

A customer commits to minimum examination volumes and pays Pro Medicus for each study processed through the platform. If volumes exceed the minimum, Pro Medicus can earn additional revenue.

This is an excellent model.

The hospital avoids a giant upfront software licence and links part of its spending to actual activity.

Pro Medicus receives recurring revenue, contract visibility and exposure to growth in customer imaging volumes.

The contracts often run for five to ten years.

That does not make the revenue completely automatic. Hospitals still need to prepare infrastructure, migrate data, connect external systems, train users and reach go-live.

A contract announcement is not revenue.

It is a promise of revenue that must first survive implementation.

This distinction matters because Pro Medicus’ recent contract values are getting rather silly.

By 1 June 2026, management said FY26 contract sales had exceeded $400 million in total contract value, more than double the level from two years earlier. Recent wins included $90 million over seven years with Beth Israel Lahey Health, $23 million over five years with the University of Maryland Medical System and another full-stack contract with TidalHealth that included cardiology.

Those are real contracts with real customers.

But the revenue arrives over years, not next Tuesday.

The financial numbers are ridiculous

I mean that as a compliment.

FY25 revenue increased 31.9% to $213 million. Net profit rose 39.2% to $115.2 million.

That produces a statutory net profit margin of roughly 54%.

Operating cash flow was $111.3 million, almost matching profit, and Pro Medicus finished the year debt-free with $210.7 million of cash and other financial assets.

The H1 FY26 result continued the pattern.

Revenue rose 28.4% to $124.8 million. Underlying NPAT increased 29.7% to $67.3 million, while the underlying EBIT margin reached approximately 73%.

The company remained debt-free and reported $221.8 million of cash and other relevant financial assets.

A 73% EBIT margin is absurdly good.

Every extra examination produces revenue, but Pro Medicus does not need another salesperson, engineer or server for every extra scan.

Revenue can grow much faster than costs.

That is operating leverage, and Pro Medicus has it in industrial quantities.

Cash conversion is also excellent.

H1 FY26 operating cash flow was $65.2 million. After deducting approximately $4.3 million of capitalised development and $0.3 million of property expenditure, my conservative free-cash-flow estimate is about $60.6 million.

That is roughly 90% of underlying profit.

Pro Medicus does capitalise some development expenditure, which makes reported operating profit higher than it would be if every development dollar were immediately expensed.

That deserves monitoring.

But capitalised development is modest relative to revenue, amortisation is reasonably close to new additions and the company still produces mountains of cash after deducting the development spending.

The accounting is not creating the business quality.

The business quality is creating the cash.

Be careful with the reported H1 profit

Pro Medicus reported statutory H1 FY26 NPAT of $171.2 million.

That number makes the underlying business look even more profitable than it is.

The result included an approximately $149 million pre-tax, non-cash fair-value gain on the company’s investment instrument in 4DMedical Limited (ASX: 4DX).

It would be wrong to subtract $149 million directly from after-tax profit because the gain was pre-tax.

It would be equally wrong to treat the gain as recurring Visage earnings.

The better number for analysing the operating business is the $67.3 million underlying NPAT.

The 4DMedical investment may produce a wonderful realised return.

It is not the same thing as a radiologist processing another examination through Visage.

Why the contract wins matter

Pro Medicus has three overlapping growth engines.

The first is winning new customers.

Each successful implementation creates a fresh stream of transaction revenue.

The second is growing alongside existing customers.

Hospital systems acquire clinics, build outpatient centres and process more imaging. When actual activity exceeds the contracted minimum, Pro Medicus earns more.

The third is selling more products through the same customer relationship.

A hospital may begin with Viewer, then add Workflow, Open Archive or Cardiology at renewal.

That last part could be particularly important.

The company’s recent renewals were reportedly signed for full terms, with higher per-transaction pricing and additional modules in some cases. By early June 2026, management said recently announced renewals exceeded $120 million.

That is expansion revenue without finding a completely new customer.

Lovely.

The next test is whether contract wins translate into the expected revenue.

Management said the Trinity rollout remained on schedule and expected a material step-up in transaction volumes during H1 FY27. It anticipated receiving around 85% of Trinity revenue and full contributions from the University of Colorado and BayCare by then.

University of Maryland and Beth Israel Lahey were expected to begin contributing later in FY27 and help build the FY28 revenue base.

This gives Pro Medicus unusually good growth visibility.

It does not remove execution risk.

I would track the date each contract was signed, the first go-live, the completion of each rollout stage and the resulting revenue.

Total contract value is exciting.

Cash in the bank is better.

Does Pro Medicus really have a moat?

Yes.

I think the moat is real, but it is broader than “fast software”.

The proprietary streaming technology matters. So do the integrations, archive, clinical workflow, customer trust, long contracts and implementation capability.

Consider what replacing Visage may require.

The hospital must migrate a huge imaging archive, rebuild interfaces, validate the new system, retrain thousands of users, obtain security approval and change clinical workflows.

It also needs to accept the risk that something goes wrong.

This software sits inside patient care.

“Close enough” is not a comforting technology strategy when the wrong examination could reach the wrong person or an urgent study fails to load.

That creates genuine switching costs.

Pro Medicus also appears unusually good at implementation.

Management says large deployments can be completed in less than one-fifth of the normal industry time. The exact comparison is difficult to verify independently, but successful rollouts at increasingly large organisations provide some evidence that its implementation system is repeatable.

There is another advantage that management sometimes calls a network effect.

I would call it a reference effect.

One hospital does not receive more direct value merely because another hospital uses Visage. This is not a social network.

But when a huge, respected health system successfully deploys Pro Medicus, the next buyer may conclude that the company can handle its environment too.

That lowers perceived procurement risk.

In healthcare technology, avoiding disaster is a feature.

Who competes with Pro Medicus?

Pro Medicus has a strong moat.

It does not have the field to itself.

Sectra offers enterprise imaging across radiology, cardiology and pathology. Siemens Healthineers has its Syngo Carbon platform. Fujifilm sells the Synapse enterprise-imaging suite.

GE HealthCare also acquired Intelerad, giving the combined business greater capital, hospital relationships and distribution.

Large competitors can bundle imaging software with scanners, maintenance agreements and other hospital technology.

They do not necessarily need to build a better Visage.

They need to build something good enough, package it attractively and offer a lower price.

Australia’s Mach7 Technologies Ltd (ASX: M7T) is a much smaller company, but it also provides enterprise-imaging technology and demonstrates that Pro Medicus is not the ASX’s only exposure to this part of healthcare software.

Management admitted during the H1 FY26 call that Pro Medicus had lost some tenders, generally because of price.

That is important.

Pro Medicus positions itself as the premium option. Its argument is that better productivity and faster implementation create a lower total cost even if the software price is higher.

I think that argument is credible.

Some procurement teams clearly disagree.

Premium pricing is a sign of strength until customers decide “good enough” will do.

Can AI replace Visage?

Not easily.

Can AI change the economics of Visage?

Absolutely.

The cartoon bear case says a hospital will ask an AI model to build a new image viewer and cancel Pro Medicus a week later.

That is not serious analysis.

Visage is a regulated, mission-critical enterprise system connected to clinical workflows, image archives and other hospital applications. Replacing it requires more than generating code.

But the opposite argument — that AI can only help Pro Medicus — is too comfortable.

AI can attack individual tasks.

It can help write and check reports. It can prioritise urgent examinations. It can measure structures, flag possible abnormalities, build integrations and improve customer support.

It may also reduce the cost of migrating data or recreating software features.

The most credible AI threat is not sudden replacement.

It is gradual unbundling.

An electronic medical record vendor might control more of the doctor’s interface. An AI company might become the layer that selects and coordinates diagnostic algorithms. Better migration tools might reduce switching pain.

A competitor may not need to match every part of Visage.

It may need to close enough of the gap to make Pro Medicus’ premium pricing harder to defend.

Why AI could make Pro Medicus stronger

Pro Medicus already owns an important part of the radiologist’s workflow.

That creates an opportunity.

AI algorithms are not especially useful when they live in 14 separate applications, each requiring another login and another interruption.

A diagnostic tool becomes more valuable when its output appears naturally within the study the radiologist is already viewing.

Pro Medicus wants Visage to become that integration layer.

Management divides AI into two buckets.

Some AI will sit inside the core platform, improving functions such as reporting, navigation or workflow.

Other diagnostic algorithms may be optional products charged on a per-study basis.

Pro Medicus can develop an algorithm internally, co-develop it with a major academic institution or integrate a third-party product.

This looks sensible to me.

There may ultimately be thousands of clinical algorithms. Pro Medicus does not need to invent all of them.

It may be more valuable to own the road than every car travelling along it.

The key investment question is not whether AI exists.

It is who captures the value when AI enters the clinical workflow.

Does the algorithm developer take most of the economics?

Does the hospital retain the savings?

Does the electronic medical record become the control layer?

Or does Pro Medicus earn additional revenue because it provides the trusted distribution and integration?

That remains unproven.

It could also be the company’s next major growth engine.

Cardiology is becoming real

Cardiology is no longer a product hiding at the back of an investor presentation.

It is appearing in contracts.

Management said Cardiology represented approximately 13%–15% of the University of Colorado contract and about 10%–12% at Vancouver Clinic.

It has also been included in new customer wins and existing-customer renewals.

The logic is straightforward.

Cardiology produces large imaging studies through echocardiograms, catheterisation, angiography and cardiac CT or MRI.

Hospitals often use separate systems for different clinical departments. Pro Medicus is offering one core imaging architecture across radiology and cardiology.

That may reduce duplicated infrastructure, make images easier to access across departments and increase the contract value per customer.

It also deepens the relationship.

A hospital using Visage across radiology, cardiology, workflow and archive has more to replace than one viewer.

Digital pathology could create another extension because digitised tissue slides can be enormous.

However, pathology is earlier.

Cardiology is becoming commercial evidence.

Pathology remains optionality.

There is nothing wrong with optionality.

Just do not put all of it into next year’s spreadsheet.

The 4DMedical deal may reveal a second flywheel

Pro Medicus has cash.

It has a highly profitable core business.

It also has something smaller healthcare companies often lack: access to major US hospital systems.

That distribution may be worth more than the cheque.

Pro Medicus invested $10 million in 4DMedical Limited (ASX: 4DX) through a hybrid instrument combining debt and equity-linked returns. The arrangement carries a 12.5% coupon and is due to mature in July 2027.

At 31 December 2025, Pro Medicus valued the instrument at approximately $159 million, creating the enormous unrealised gain recorded in H1 FY26.

That is one heck of a result from $10 million.

It may become even better or substantially less valuable before maturity because the final payoff depends partly on the 4DMedical share price.

The more interesting point is why Pro Medicus might be a valuable investor.

A small medical-technology company can develop a clever product but still struggle to:

- obtain regulatory clearance;

- integrate with hospital systems;

- validate the technology;

- reach procurement teams;

- train clinical users; and

- achieve broad commercial adoption.

Pro Medicus can potentially help solve those problems.

In return, it can negotiate attractive investment terms, add another product to Visage and earn a share of the commercial upside.

Echo IQ shows how the model could develop

In June 2026, Pro Medicus signed a binding heads of agreement with Echo IQ Limited (ASX: EIQ).

The proposed arrangement included an initial $10 million secured convertible-note investment, an option for another $10 million after an FDA milestone and a US reseller relationship covering Echo IQ’s cardiovascular diagnostic technology.

Pro Medicus said it intended to offer Echo IQ technology to Visage 7 Cardiology customers as part of a curated AI suite. Definitive legal agreements were still being negotiated when the arrangement was announced, so it should not yet be treated as a completed investment and reseller deal.

This is the potential flywheel:

Pro Medicus generates excess cash.

It invests in a useful healthcare technology on favourable terms.

The technology is integrated into Visage.

Pro Medicus distributes it to customers.

The partner gains commercial access.

Pro Medicus earns product revenue, investment returns or both.

Visage becomes more valuable.

That is a powerful model.

It is not yet a proven model.

One excellent 4DMedical outcome does not make Pro Medicus the Berkshire Hathaway of medical imaging.

A spectacular first investment can also create overconfidence. Management may become more willing to write cheques, accept regulatory risk or confuse a rising partner share price with commercial success.

I would judge each investment by the product integration and recurring revenue it creates.

Paper gains are lovely.

A stronger moat is better.

Management alignment is exceptional

Co-founders Sam Hupert and Anthony Hall together own roughly 46% of Pro Medicus.

That is genuine alignment.

Their wealth is overwhelmingly connected to long-term value per share rather than next year’s bonus.

The company’s history also supports the case for disciplined management.

The 2009 Visage acquisition transformed the business. Management then spent years improving and commercialising the technology rather than buying a collection of unrelated software companies.

Pro Medicus has used little debt, issued relatively few new shares, increased dividends and maintained a tight cost base.

This is capital allocation with fewer moving parts than a Swiss watch.

There is another side.

Founder alignment can become founder dependence.

Hupert remains central to strategy, customer relationships, product positioning, investor communication and capital allocation.

The market is not only valuing Visage.

It is also valuing Hupert’s judgement.

That makes succession important.

Pro Medicus has experienced technical leadership beyond its founders, including the team in Germany that develops Visage. I do not think the intellectual property sits inside one person’s head.

Still, the company has not clearly shown investors what a post-Hupert leadership model would look like.

Senior transitions are already beginning.

Clayton Hatch, a long-serving executive and former CFO, is due to leave his operations and investor-relations role in August 2026 to join Artrya Limited (ASX: AYA) as CFO. Artrya is developing AI-based coronary-imaging software.

One departure is not a crisis.

It is a reminder that Pro Medicus must become more institutional without losing what made it special.

Easy to say.

Hard to do.

What could go wrong?

The bear case is better than many shareholders admit.

The most obvious risk is valuation.

I will return to that shortly.

Pro Medicus could also lose more tenders on price. A competitor may improve its cloud architecture or bundle an adequate product with other hospital technology.

Large implementations may take longer than expected because customers are not ready, even when Pro Medicus has done everything right.

The Australian dollar can reduce reported growth when US-dollar revenue is translated back into Australian dollars.

Cardiology may grow more slowly than expected. Pathology may take years. AI algorithms may generate more value for their developers or hospital customers than for Pro Medicus.

Margins may also have limited room to improve.

The CFO told analysts not to expect the EBIT margin to keep shooting dramatically higher from its already extraordinary level.

That means future profit growth will depend mostly on revenue.

Pro Medicus may also need more spending on cybersecurity, implementation teams, clinical validation, regulatory work, customer support and management depth.

A serious outage or security incident would be particularly damaging because customer trust is part of the moat.

Then there is succession.

A poor transition away from the founders could weaken culture, product focus and capital discipline.

Finally, strategic investing could become a distraction.

The company has earned the right to test the model.

It has not earned an unlimited licence to become a listed healthcare venture fund.

What does the Pro Medicus share price assume?

At the 15 July 2026 closing price of $192.62 and approximately 104.46 million shares, Pro Medicus had an estimated market capitalisation of $20.1 billion. This is my calculation using the market price and reported share count.

The reported statutory H1 profit is not useful for valuation because of the 4DMedical gain.

A rough illustration is to annualise the H1 underlying NPAT:

$67.3 million × 2 = $134.6 million

Then:

$20.1 billion ÷ $134.6 million = about 149 times annualised underlying earnings

This is not a forecast P/E ratio.

Management expected H2 FY26 to be stronger, and FY27 should benefit from more large implementations.

Annualising a single half ignores that growth and seasonality.

The calculation has one purpose.

It shows how much success the valuation still requires.

The cash-flow picture is similar.

Annualising my conservative H1 free-cash-flow estimate produces approximately $121 million.

Against a $20.1 billion market capitalisation, that is an illustrative free-cash-flow yield of around 0.6%.

Again, not a forecast.

It is a starting-point reality check.

Suppose Pro Medicus grows annual profit of roughly $135 million at 25% for an entire decade.

Year-10 profit would be approximately $1.25 billion.

That would be a phenomenal result.

The investor’s return would still depend on what valuation the market applies ten years from now.

This is the problem with paying an extraordinary multiple.

The company can deliver an extraordinary outcome and the shareholder can still receive an ordinary return if too much was paid at the beginning.

A falling share price is not proof of value.

It only tells us the old price was higher.

What the market may be misunderstanding

The lazy bear case is that AI will build a cheaper Visage and destroy Pro Medicus.

I do not believe that.

A new feature is not a replacement for a regulated and deeply integrated enterprise system.

The lazy bull case is that Pro Medicus is the best company on the ASX, so valuation does not matter.

I do not believe that either.

Every valuation is a set of expectations wearing a number as a hat.

The market may be underestimating how difficult Visage is to replace.

At the same time, it may be overestimating how long Pro Medicus can maintain growth near its historical rate.

I also think investors may focus too heavily on the 4DMedical paper gain.

The bigger long-term opportunity is using Pro Medicus’ cash, customer access and integration capability to distribute useful healthcare technologies.

That could produce recurring revenue and strengthen Visage.

A one-off investment gain is nice.

A repeatable distribution advantage could be worth far more.

Buy, hold or sell?

I will put it this way.

I would not buy Pro Medicus simply because the Pro Medicus share price has fallen.

Shares can fall 40%, remain expensive and then fall again. Markets are rude like that.

The buying case is the business quality.

Pro Medicus has an outstanding product, long customer contracts, strong renewal evidence, high cash conversion, no debt and significant founder ownership.

Signed contracts should support FY27 and FY28 growth. Cardiology is increasing the revenue opportunity per customer. AI distribution and strategic investments provide genuine optionality.

An investor willing to accept a high valuation for rare quality may reasonably decide the business deserves a place on a long-term watchlist or in a diversified portfolio.

The holding case is also strong.

Long-term shareholders own one of the ASX’s most impressive companies. Selling merely because a conventional multiple looks frightening has historically been a costly strategy with exceptional compounders.

But “it has always looked expensive” is not analysis.

A shareholder still needs to monitor whether revenue, customer expansion and competitive evidence continue justifying the valuation.

The avoiding or selling case is strongest for investors who need a wide margin of safety.

At this price, Pro Medicus does not need to become a bad company for returns to disappoint.

Growth merely needs to become more ordinary.

I would focus on a small number of signals:

- revenue from Trinity, UCHealth and BayCare;

- renewal length and transaction pricing;

- tender wins and losses;

- cardiology’s share of new contracts;

- paid AI adoption;

- cash flow after all development expenditure;

- founder and executive succession; and

- the commercial returns from strategic investments.

I would become more positive if the valuation provided more room for mistakes or if Cardiology, AI distribution and partner products became meaningful recurring revenue sources.

I would become more cautious if contract terms shortened, pricing weakened, implementations slipped or strategic investments expanded faster than the supporting commercial evidence.

Final thought

I think Pro Medicus Limited (ASX: PME) may be the best operating company on the ASX.

Its profit margins are real.

The cash is real.

The customers are real.

The contract wins are real.

Its founders have an enormous amount of their own money travelling beside ordinary shareholders.

The moat is also more substantial than fast software.

Visage is embedded inside difficult, regulated and mission-critical clinical workflows. Replacing it requires more than an AI model and an enthusiastic press release.

The company’s next act may be even more interesting.

Pro Medicus can potentially use its balance sheet, cash flow and US distribution to help smaller healthcare companies cross the gap between clever technology and commercial adoption.

4DMedical and Echo IQ provide early evidence of what that model could become.

Still, the Pro Medicus share price demands a long period of excellent execution.

Maybe management delivers it.

I would be very careful betting against this company.

I would be equally careful assuming any company is worth any price.

Business quality and investment quality are close relatives.

They are not twins.

I still own the Pro Medicus shares I first bought in 2017 — nearly 10 years ago.

Log in to the Rask platform to view my latest Pro Medicus valuation and investment notes.