Qoria’s quarterly update spooked investors, why was it sold off and is the takeover all its cracked up to be?

It’s been a volatile period for Qoria Ltd (ASX: QOR) shareholders.

In late January, the company delivered a quarterly update that looked solid on the operational metrics, but the details provided a few more troubling signs. A share price sell-off ensued before an unusual takeover proposal landed.

So what does it all mean?

The mixed quarterly report

At a glance, the quarterly report looked good.

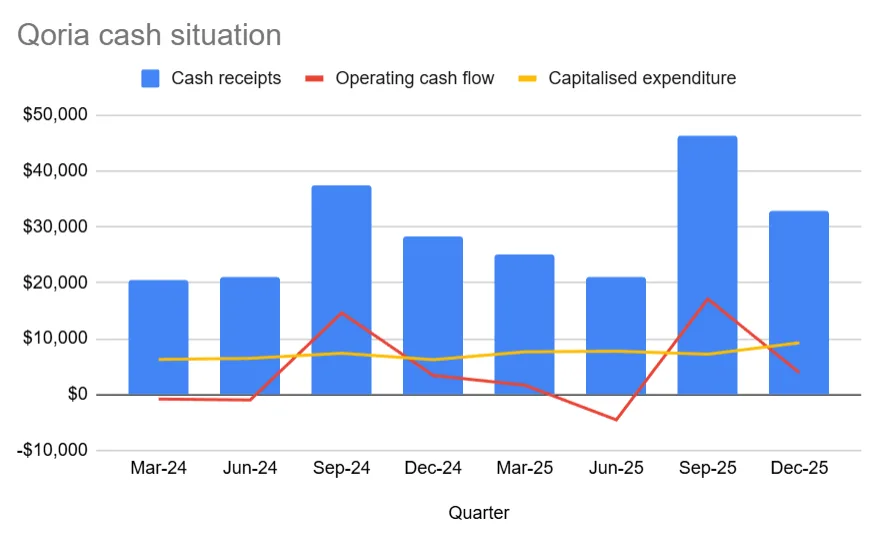

Operationally, Qoria reported that Annual Recurring Revenue (ARR) had passed US$100m, and that it exited December 2025 with AUD$149m in ARR, representing ~20% growth compared to last year. Growth was broad-based: K-12 added AU $4.6m of gross ARR for the quarter, and Qustodio added AU $2.1m of net ARR. Gross margins sit at 92% and net retention at 102% over the last 12 months.

It wasn’t all sunshine and rainbows.

By the time you reach page 26 of 31 page quarterly report (the length perhaps a red flag in itself) you get to the nitty gritty of the numbers, beyond the flashy colours and charts. The company is highly seasonally driven, closely aligned with the US & UK school years. So while the ~$4 million in operating cash is a big drop off from Q1, the December quarter isn’t typically a significant cash generator in the Northern Hemisphere and improved on the same time last year.

It’s important to look beyond operating cash flow. Qoria capitalised ~$8 million in development costs, making it $13.2m for the year. FX played its part, with the weakening US dollar reducing net ARR by $4.5m and raising cash costs by $1.5m, implying a ~$3m negative cash EBITDA impact.

Q1 is the golden goose of cash flow. So if we see a similar pattern to 2025, plus increasing development costs. Are we approaching a cash shortfall?

Add to that net debt of $32 million and any hiccups are magnified.

The takeover

The get-out-of-jail card has arrived, or has it?

In early February, Qoria announced that Aura, a U.S.-based subscription platform for broader consumer digital security, would acquire 100% of Qoria via a scheme. As part of the arrangement, Qoria shareholders will receive 1 CDI (A CDI gives investors the same beneficial interests in foreign companies as holding these shares on a foreign exchange) for every 17.2 Qoria shares.

It’s not your everyday capital transaction, supported by a 61-page presentation.

Existing Aura shareholders (a private company) are tipping in $75 million in equity at a share price of $12.38. The arithmetic, dividing the $12.38 placement price by the 17.2 shares that Qoria holders would receive, gives a deemed share price of $0.72. Qoria shares rose early after the trading halt, but have yet to reach $0.72 and are languishing in the low 40s.

There could be a number of reasons for this

It’s an unusual situation in that Aura is setting the price as a private business, using its $12.38 per share.

There’s no public market for Aura; the market price is less transparent than for something like Qoria, which trades daily and has its value set by the marketplace. We only know that investors have committed capital at that price in a private placement, so you’re relying on key investors’ assessment that the price is accurate.

The implied value of the combined group is ~$3 billion.

This would be pushing the company into the top indexes on the ASX, bringing in passive money and potentially boosting valuation. The cynic in me would suggest that might be one reason for a US technology company to backdoor list on the ASX, to get an exit and valuation boost, compared to the usual path of high quality technology companies that list on the Nasdaq.

The board’s support for the deal was explicit, with a unanimous recommendation subject to “no superior proposal” and an independent expert ticking off shareholder value. That is one way to get through a quasi-cap raise.

The lessons and what to watch from here

While the most attractive numbers are always going to be at the front of the presentation, it’s always worth skipping through the gloss and checking the hard numbers first.

I’m not suggesting the Qoria is actively trying to deceive the market, and it’s natural for them to point out their successes. Ultimately, cash is king, and if you’re burning more than you’re earning, the market will sniff out the need for a raise. Then, when that raise appears in the form of a questionable merger, you have to begin to ask questions as to the motives of those involved.

To me, this acquisition feels a little odd. There’s every chance I’m wrong, and it’s a success and moves higher into the index and picks up passive flows, but just do your due diligence.