Unless you’re in the market for a unit or apartment, Sydney and Melbourne home prices are a young person’s biggest money worry.

Below, I’ll reveal 7 simple tips that anyone can use to take the worry out of buying a shack in the burbs.

-

Increase your timeline, lower stress

We all underestimate what we can achieve in 5 years and overestimate what we can get done in 1 year. Everyone does it.

But no-one wants to hear, “keep saving guys, you’ll get there in a couple of years.” Especially when your parents are asking you 101 questions when you get home from work or uni. “What do you want for dinner?” “How was your day?” “Did you learn something new?”.

You’re thinking: ‘Give me a break.’

But the cold hard truth is this: unless you want to rely on your parents for a handout (hello, Bryce Walker from 13 Reasons Why) you need to get your savings in order.

And that’s best done with a two-to-three year plan.

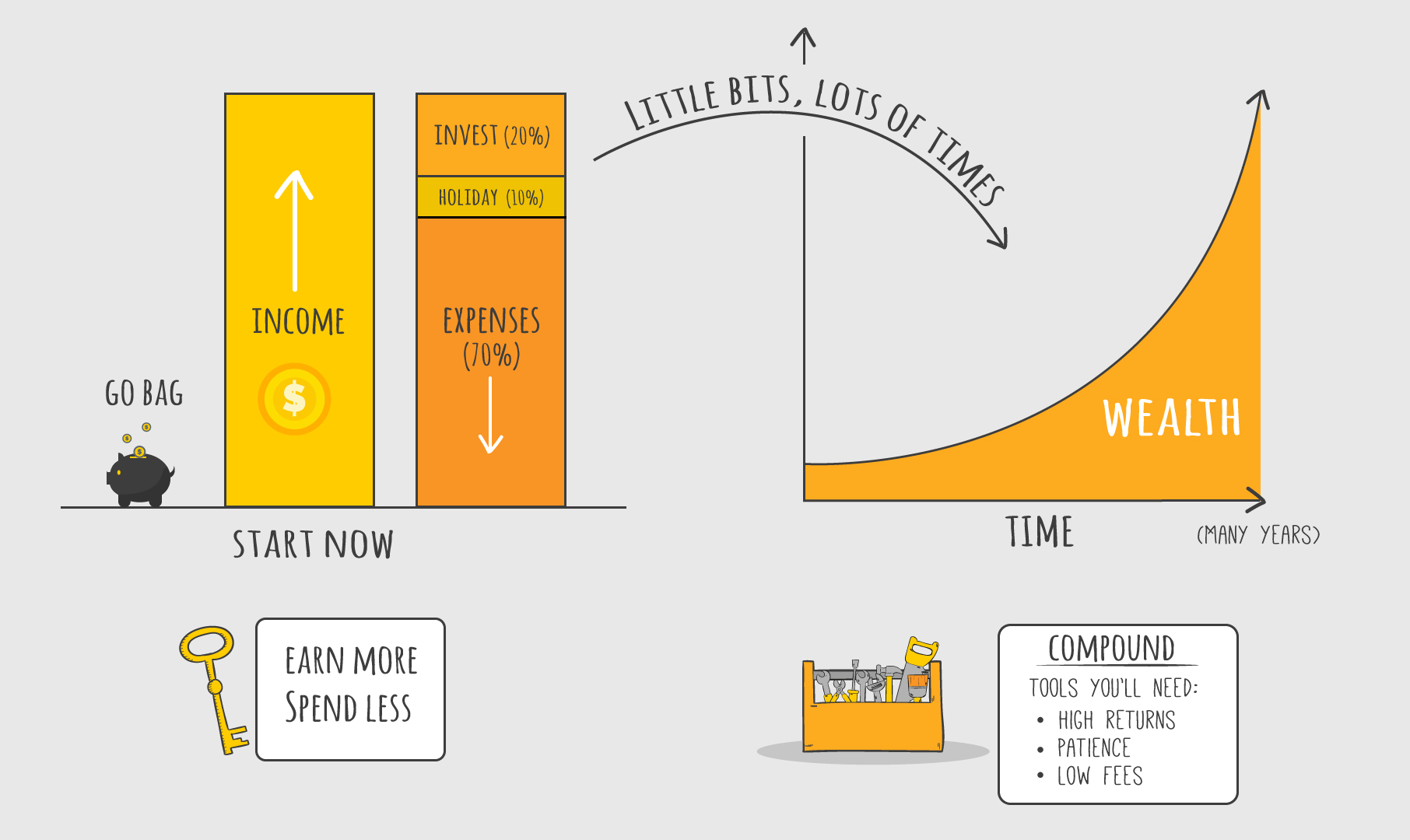

Save more than 20% of your income in a high-interest account and plan to buy in years — not months — from now.

Having a longer-term plan will lower your stress and provide light at the end of the tunnel.

-

The market is not getting away from you

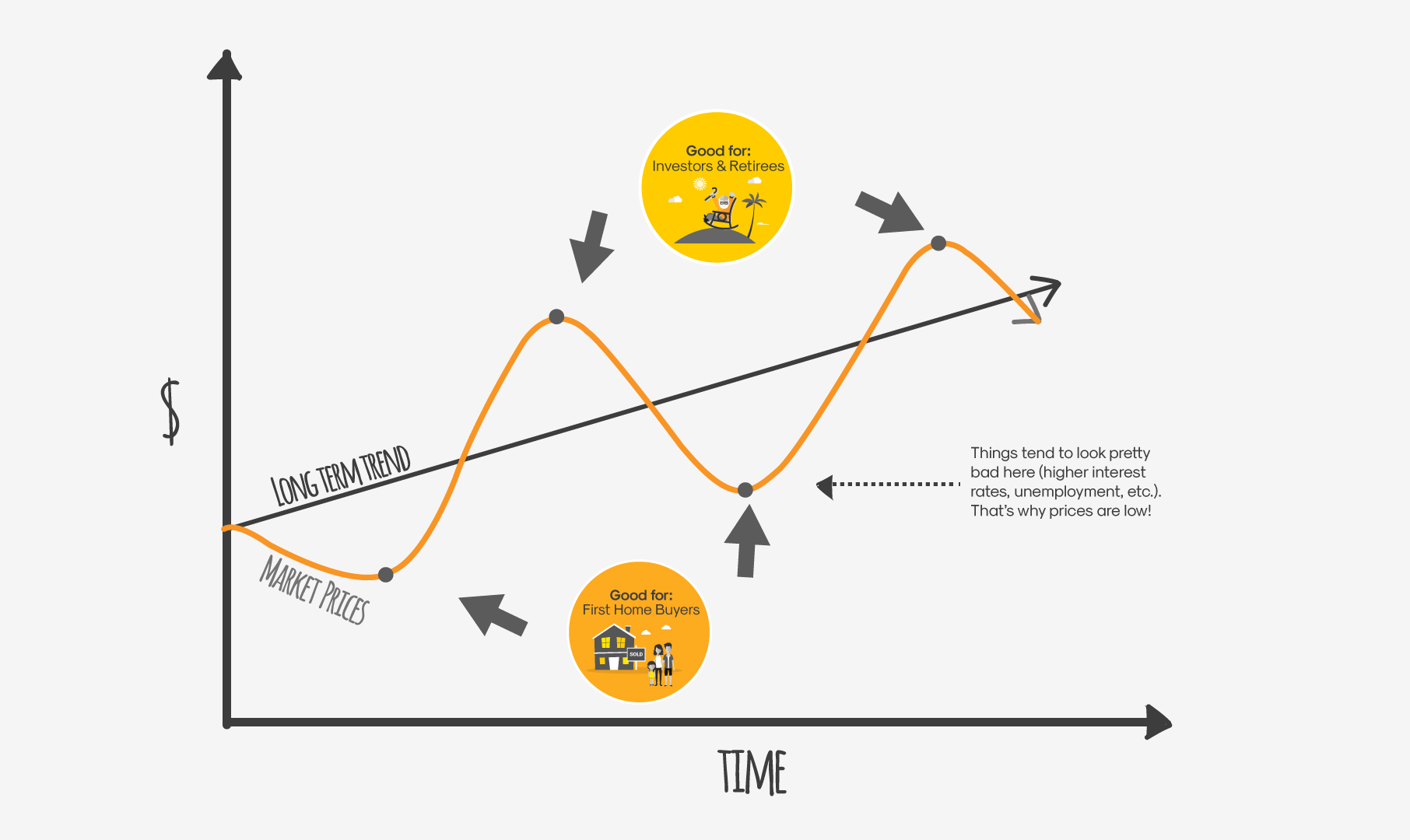

Prices are rising, sure. And, over time, house prices have a tendency to increase — if history is anything to go by.

But, house prices are not guaranteed to double every 7 years.

You may not realise it given the price increases over the past 10 years but property markets are cyclical. What that means is even though they rise over time, there will be times when it is much better to be a buyer than an owner of a property. Here’s a snippet from Rask Invest:

The moral of the story? Patience doesn’t lose you money. If you map out your savings plan and it just ain’t workin’, you have a few options:

- Get a second job

- Put off your timeline to 5+ years and rent and invest your money elsewhere

- Invest in yourself. Read books, brown nose or study on the side to get a promotion at work (or change jobs!). Here’s a secret: Your boss pays you the minimum amount to keep your around and you do the minimum not to be fired. It will take time but make yourself invaluable by investing in your knowledge and skills — good things will follow.

-

Don’t buy at auction

Are you the guy or gal who throws fish and chips to seagulls?

Ugh.

A property auction is the human equivalent. Everyone is squawking bids and falling over themselves as the agent and owner sit there laughing.

Auctions are NOT designed for the buyer — but especially first home buyers.

They’re designed to get the best price for the current owner by making people bid with emotion.

So, call the agent and give them your best price a day or two before the auction

. If the place doesn’t sell at auction call them again. If it’s your best price you likely wouldn’t have got the place anyway.

A house is the biggest financial commitment most of us will ever make.

Be confident, be bloody ruthless. But be tight with your cash and don’t put yourself in a situation in which you will easily go over your budget.

-

Avoid taking risks to save “quickly” for a deposit.

Investing in shares, bitcoin and ETFs involve risk. Risk means: ‘things can go wrong quickly and you can lose — BIG time’.

Imagine if you chucked your $10k or $20k deposit in bitcoin at the beginning of the year. The time when, as Adam Sandler’s character from Billy Madison says (with a wet patch on his groin), “everybody is doing it, it’s the coolest”.

Bitcoin is down 50% so far in 2018, according to Coinbase data.

FOMO, or the ‘fear of missing out’, is a combination of envy and jealousy. They are two things that lead to financial mistakes and heartache.

Don’t panic. Keep saving safely, you’ll get there.

-

Rent-vesting can work

This is not something I recommend to everyone. However, buying in a cheaper suburb and renting a modest home in a place you want to live can work — on paper.

But it’s not without risk. If you are considering this strategy avoid stretching yourself with excessive debt.

By that I mean, make sure your investment property’s rent covers all of the costs of owning and maintaining the property — not just the loan (aka negative gearing).

That should provide some cushion if the you-know-what hits the ceiling fan.

-

The Aussie dream is not everything it’s cracked up to be.

I’ve interviewed multi-millionaire investors and business people. None of them got rich via property. For most Aussies our financial lives go as follows: Work hard for someone else, save something, borrow.

But here’s the thing about that.

Money can empower you if it works for you.

Not if you work for money. There’s a difference.

That might sound bizarre, wishy-washy or even intimidating.

But if you commit to investing in your financial knowledge, even just an hour or two each week, you will learn how to empower yourself.

Once you realise this, the weight of having to buy a property will lift from your shoulders.

Ask yourself: Do people with a massive mortgage really seem happy about it?

They might tell you they are happy. But being forced to stay in the same job, put off experiences like holidays and pay the bank bucket loads of interest does not sound very empowering to me.

It’s not a bad thing to own a property — I think it’s great. But if it’s done wrong, it can be a financial and lifestyle liability masquerading as an asset.

-

Have a budget

What a climatic end to this article!

You: “Have a budget? After all that, you say ‘have a budget?!'”.

Most young people I talk to don’t keep track of their finances. People in their late 20’s and early 30’s have just begun to get some serious dough in their pay packet.

And keeping track of spending is a boring — and often scary — thing to do, right?

You may not be able to save 20% of your income, $1,000 a month or even $50 a fortnight.

But if you want to supercharge your finances and get into your own home sooner, some hard choices must to be made. Add up one month of your income and expenses from your most recent bank statement. How much are you saving?

If you can’t save 10% to 20% of your income for long-term goals (like buying a house) start with 1% this month, 2% next month and so on.

I like to think about it in terms of your day-to-day. If you’re flipping burgers at Maccas, a 10% savings rate is the same as keeping one in 10 burgers for your future. If you work a 40 hour week, four of those 40 hours belong to you and your future self.

Stick to your savings. You will get there. It’s those savings that will change your life.

Next stop: Financial Freedom

I like property as much as any other investor, but it’s out of reach for many Aussies. That’s why I like to invest most of my money in other places.

If you want to know exactly how I do it — and the exact steps I follow — you can download my free Ebook when you join the Rask Group Investor Club Newsletter. It’s free to join. I called it “What Warren Buffett’s Investment Checklist Can Teach Aussie Investors”. It’s a great introduction to investing.