Artificial intelligence is often framed as a story about software, algorithms and increasingly powerful semiconductors, but that view is starting to evolve.

That framing made sense in the early stages of the AI cycle, when attention centred on model breakthroughs and the computing power required to train them, but the narrative is now broadening. As AI moves from experimentation into industrial-scale deployment, the conversation is shifting toward the physical systems behind it.

The systems supporting this technology are becoming larger, more energy intensive and more physical, spanning data centres, power infrastructure, cooling systems and advanced manufacturing equipment, all of which rely on real-world inputs.

The materials behind the machines

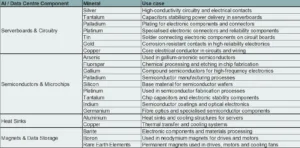

Rare earth elements, once viewed as niche industrial inputs, are now embedded across many of the machines that power modern computing, from semiconductor manufacturing tools to high-precision motors used across data centre infrastructure.

As artificial intelligence scales from a software breakthrough into a global industrial system, the materials inside that hardware are becoming just as important as the code itself.

In other words, the future of artificial intelligence is being shaped not only by code, but also by chemistry.

AI hardware depends on more than silicon

When investors think about AI hardware, the focus usually lands on GPUs, advanced semiconductors and the companies designing them. But every layer of the semiconductor manufacturing process relies on extremely precise physical systems, many of which depend on rare earth materials, something often overlooked in investor discussions.

Permanent magnets made with neodymium, praseodymium, dysprosium and terbium are used across high-precision motors that control wafer handling, lithography equipment, ion implantation systems and vacuum pumps. These magnets provide extremely stable magnetic fields and motion control, allowing chip manufacturing equipment to operate with the accuracy required for advanced node production, where even minor deviations can be critical.

The importance of these materials extends beyond chip fabrication. Rare earth magnets are also used in cooling systems, robotics, electric motors and power infrastructure that increasingly sit inside modern data centres.

What this means in practice is that AI hardware is not simply a silicon story, despite how it is often presented. As AI scales into real-world deployment, the industry is becoming increasingly dependent on a broader set of industrial inputs that sit well beyond traditional technology sectors.

Source: USGS, IEA, US Department of Energy, Semiconductor Industry Association

A supply chain shaped by geopolitics

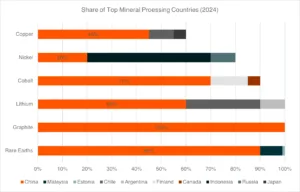

The second dimension of the rare earth story is geopolitical. Rare earth minerals themselves are not particularly rare in geological terms, with deposits found across regions including Australia, Brazil, India and China. The challenge lies in what happens after extraction, where complexity increases significantly.

Processing and refining rare earths into usable materials is technically complex, environmentally challenging and capital intensive. Over several decades, China has built dominance across this midstream stage of the supply chain. Today it controls the majority of global refining capacity and an even larger share of magnet production, giving it outsized influence over the supply chain.

That concentration means the rare earth ecosystem behaves less like a typical commodity market and more like a strategic industrial system, where policy can shape outcomes.

Recent export restrictions and licensing requirements highlight how quickly the supply chain can become a geopolitical lever. Materials that once sat quietly in industrial markets are now part of broader conversations around technology security and economic resilience.

Source: Benchmark Mineral Intelligence, IEA, World Bank

The AI build-out is lifting the materials stack

At the same time, demand is accelerating.

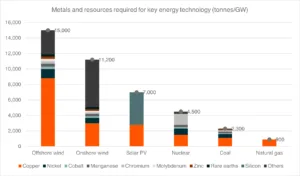

Artificial intelligence is one of the most capital-intensive technology cycles in decades, requiring enormous physical infrastructure. Training clusters, inference systems, hyperscale data centres and semiconductor fabs all require significant amounts of equipment, and each layer carries embedded materials demand, creating a ripple effect across supply chains.

Copper is needed to carry electricity through increasingly dense data centre environments. Aluminium supports cooling systems and structural components. Rare earth magnets sit inside motors and robotics, while battery materials support energy storage systems that stabilise power supply.

This is not unique to AI. Many modern energy systems, particularly renewable infrastructure, are already highly materials intensive. What AI is doing is adding another powerful layer of demand on top of that existing trend.

The expansion of AI infrastructure is beginning to pull the entire materials stack higher, from mining through to advanced manufacturing. Investment in data centres alone is expected to reach into the trillions over the coming decade, pushing demand further upstream.

From niche inputs to strategic assets

The AI build-out is now spreading beyond software and semiconductors into the materials that enable them, highlighting a broader investment narrative.

Advanced chips require specialised manufacturing equipment, while the infrastructure supporting AI workloads demands vast amounts of power, cooling and connectivity. Beneath all of this sits a layer of critical materials that quietly enable the system.

Copper, uranium and rare earth elements are becoming increasingly central to how this infrastructure is built and maintained. As AI moves from a software breakthrough into a global industrial build-out, the investment opportunity is expanding beyond compute and into the materials that power the system, broadening how investors think about exposure.

The future of AI may be digital, but it is ultimately built from the periodic table.

Source: IEA, Goldman Sachs Research

As AI moves from a software breakthrough into a global industrial build-out, the investment opportunity is expanding beyond compute and into the materials that power the system. This broader exposure is reflected across areas such as copper through the Global X Copper Miners ETF (ASX: WIRE), uranium through the Global X Uranium ETF (ASX: ATOM), and critical minerals including rare earths through the Global X Green Metal Miners ETF (ASX: GMTL).