Thinking about starting your FIRE journey and chasing financial independence? One of the most important steps is knowing your Financial Independence (FI) number—the figure that shows how much money you’ll need invested to live comfortably without working. Here’s what it means, how to calculate it, and how you might reach it sooner.

In short, your FI number is the amount of money you’ll need to live comfortably without relying on regular employment income. Once you reach your FI number, you can more or less consider yourself financially independent. Your savings or investments are generating sufficient passive income to cover your day-to-day expenses (as well as a few discretionary costs, should you choose).

It’s important to know your FI number because it gives you a tangible goal to work towards. It allows you to figure out which saving and investing strategies to adopt to hit your target, and helps you undertake long-term financial planning. Along your journey to financial freedom, you can consistently check in to ensure you’re still working towards your aim rather than meandering towards an arbitrary figure.

One thing to note is that your FI number is entirely personal. It depends on numerous factors around your financial situation and lifestyle, and the lifestyle you hope to enjoy when you achieve financial freedom. This is why your FI number is likely to be entirely different from someone else’s.

What factors contribute to my FI number?

Determining your FI number might seem as simple as plucking a number from your head that seems like a decent amount to live off. But the process isn’t quite that straightforward. Instead, there are lots of different considerations that impact your FI number – like what your current finances look like, how much you spend, and how you foresee your early retirement.

Here are the factors that contribute to your FI number:

-

Current living expenses. Your costs may be the biggest factor in calculating your FI number. This is because they impact how quickly you can achieve FIRE, and the amount you’re aiming for will need to cover your ongoing expenses come retirement.

-

Projected lifestyle and expenses. Beyond the costs you face now, you’ll also want to consider how your expenses could change once you retire. You may choose to live more frugally to ensure your money goes the distance, or perhaps you see yourself spending more on travel and hobbies.

-

Investment returns. Investing is a crucial part of reaching FIRE, so determining both your current and potential ROI is important. The former helps figure out when you may achieve financial independence, while the latter gives you an idea of how much passive income you may earn once you stop working.

-

Debt. Debts like your mortgage, student loan, and car loan impact your FI number because you may need to continue paying these off once you retire early.

-

Inflation. Be mindful that inflation impacts your finances because the real value of your money is reduced by the natural increase in the cost of living. As such, it’s important to consider the effects of inflation rates on your FI number.

-

Other sources of income. Beyond your savings, you may have other forms of income to keep you afloat during retirement. These include rental income from investment properties, dividends, part-time work, superannuation once you reach preservation age, and the Age Pension once you qualify for it.

-

Your risk appetite. More risk-averse investors may prefer to calculate their FI number using a higher projection of annual expenses, such as 30x. This can help cover any changes in expenses or market fluctuations and may provide more of a financial buffer.

How can I calculate my FI number?

Wondering how you can determine your FI number? There are several methods for doing so. Don’t forget, though, that the number you end up with is merely a ballpark figure. Things like inflation and changes to your lifestyle and expenses can shift your FI number, so treat the final calculation as a rough guide.

The 4% rule

The 4% rule suggests you can safely withdraw around 4% of your portfolio each year while keeping your money intact for roughly 30 years. To calculate your FI number, estimate your annual retirement expenses and divide that figure by 0.04.

For example, if you expect to spend $50,000 per year, your FI number would be $1.25 million.

The rule comes from the Trinity Study (1998) and is a popular benchmark, but it has limitations. It was based on US data, doesn’t account for superannuation or Australian inflation, and assumes your expenses stay the same throughout retirement. It’s best used as a rough guide—not a guarantee.

The 25x rule

Similar to the 4% rule, the 25x rule assumes you’ll need 25 times your annual expenses to retire early. Using the same $50,000 figure, that means $1.25 million. Both rules give a simple framework, but neither should be treated as exact.

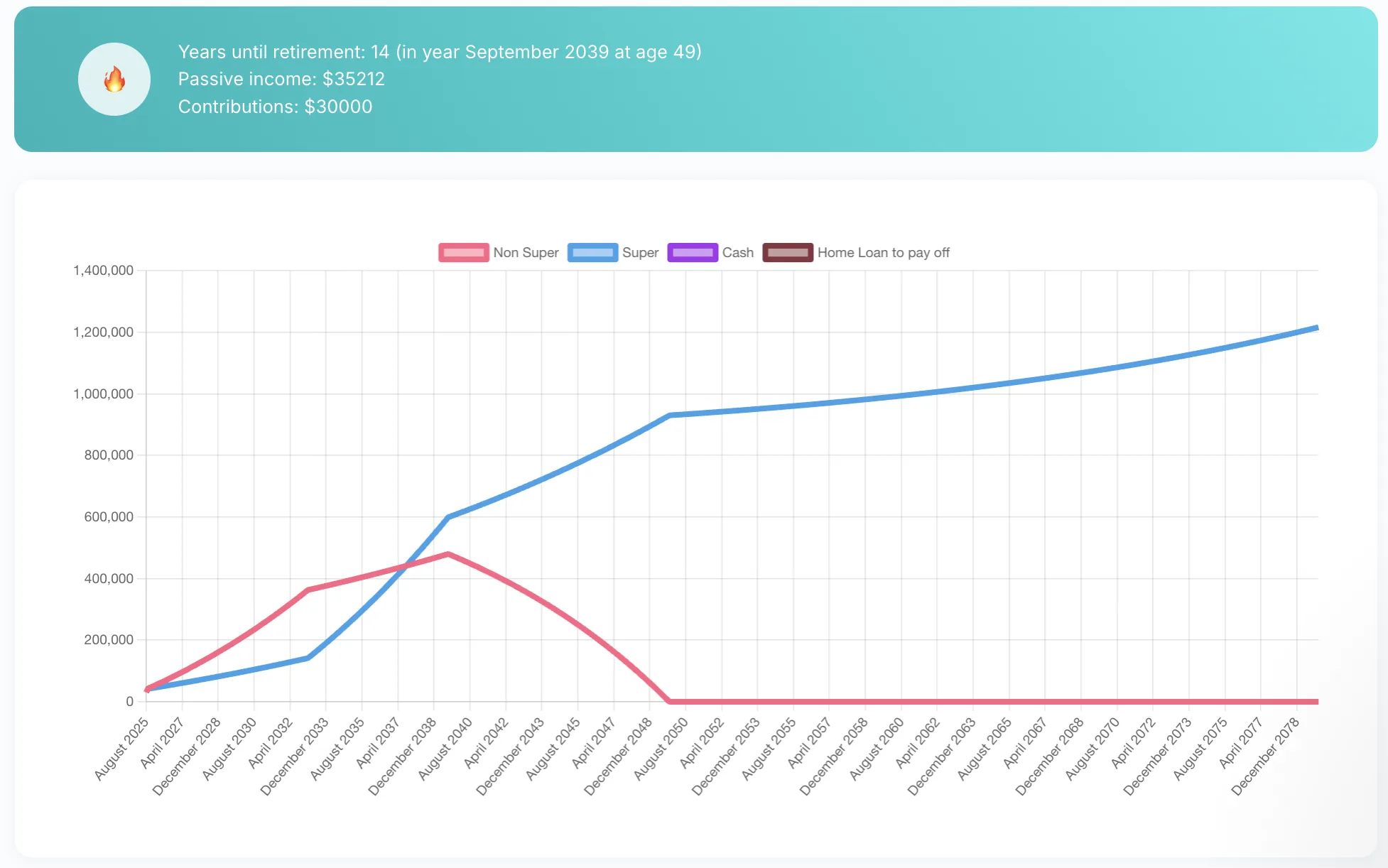

Pearler’s Financial Independence Calculator

Rather than fiddling about with formulas, Pearler offers a handy Financial Independence Calculator to help you determine your FI number. Simply plug in some details about your financial situation and investments and you’ll receive an estimate to work towards.

Just remember that, as with any online tool, the Financial Independence Calculator shouldn’t replace the expertise of a professional. If you’re facing a financial decision, consider reaching out to a licensed financial adviser for tailored advice. In saying that, Pearler’s Calculator is a great place to to get a quick general view of your financial independence projection. Have a look at an example below!

Case studies

Let’s look at the FI number in action using a couple of (purely fictional) case studies.

John, 23, software engineer

John has a decent income of $120,000 but lives a pretty moderate lifestyle and doesn’t have any kids. He only spends about $40,000 a year on expenses like rent, food, transport, travel and entertainment.

Using the 25x rule, John determines that his FI number is $1 million. John saves 50% of his income and invests in a diversified selection of assets. His aim is to eventually live off the dividends from his portfolio, although he understands that his investments can’t guarantee a return. Because of his aggressive savings strategy and investment choices, it’s projected that he’ll reach his FI number in around 12 years – meaning he could retire at 35.

Genevieve, 30, marketing consultant

Genevieve’s income isn’t quite as high as John’s. As a marketing consultant, she earns $80,000 per year. However, her expenses are slightly lower – around $30,000 annually.

She uses the 4% rule to figure out her FI number, which ends up being $750,000. To achieve her goal, she wants to save $50,000 every year (relying on an average annual return of 7%) and invest in a mix of assets including stocks and bonds. If she can stick to her plan, she reckons she’ll be able to retire within 15 years.

How can I achieve my FI number sooner?

If you’re keen to reach financial independence earlier, there are a few strategies you can consider to try and accelerate the process.

-

Reduce your living expenses. Living more frugally now may help you save money, which could be put into your savings or invested. Even small changes can add up to significant amounts over time. The same goes for your living expenses in retirement. You might be able to downsize to reduce your accommodation expenses, or you may find your transport costs go down when you’re no longer commuting.

-

Save more. Your FI number is all about how much you can save to comfortably retire. See if there are ways to save more, like comparing your account’s interest rate to other options, curbing discretionary spending or starting a side hustle.

-

Evaluate your investing strategy. Periodically assess your current investing strategy and consider whether it is meeting your goals. You could also look at different sources of passive income to supplement your retirement savings.

Find out what financial independence could look like for you — use Pearler’s Financial Independence Calculator and see how close you are to your FI number.