Wesfarmers Ltd (ASX: WES) has three major growth drivers, under the surface… that you probably never knew. In this article, I’ll explain what they are, and why they matter.

Wesfarmers share price

What do a lithium mine, bargain home products, and a couple of 4×2’s have in common?

Not a whole lot.

But…

You can get plenty of exposure as an investor by holding shares in Wesfarmers Ltd (ASX: WES), the Aussie conglomerate. A quasi-private equity fund, it provides a combo of growth and defensive exposure, and an alternative to other listed players.

In the space, we’ve seen Washington H Soul Pattinson & Co Ltd (ASX: SOL) recently propose to merge after 56 years. And Seven Group Holdings (ASX: SGH) has continued to trudge higher.

So is this the time to invest in Wesfarmers shares?

Wesfarmers’ ability to allocate capital and churn out returns has earned it an inflated valuation compared to the market. Given the consistency of profit and return on investment, it may be worth it.

Below, I’ll take a look at three reasons why I like Wesfarmers…

3 reasons Wesfarmers could outperform

The chart above comes from Tikr.com, the best tool for financial data and fundamental analysis.

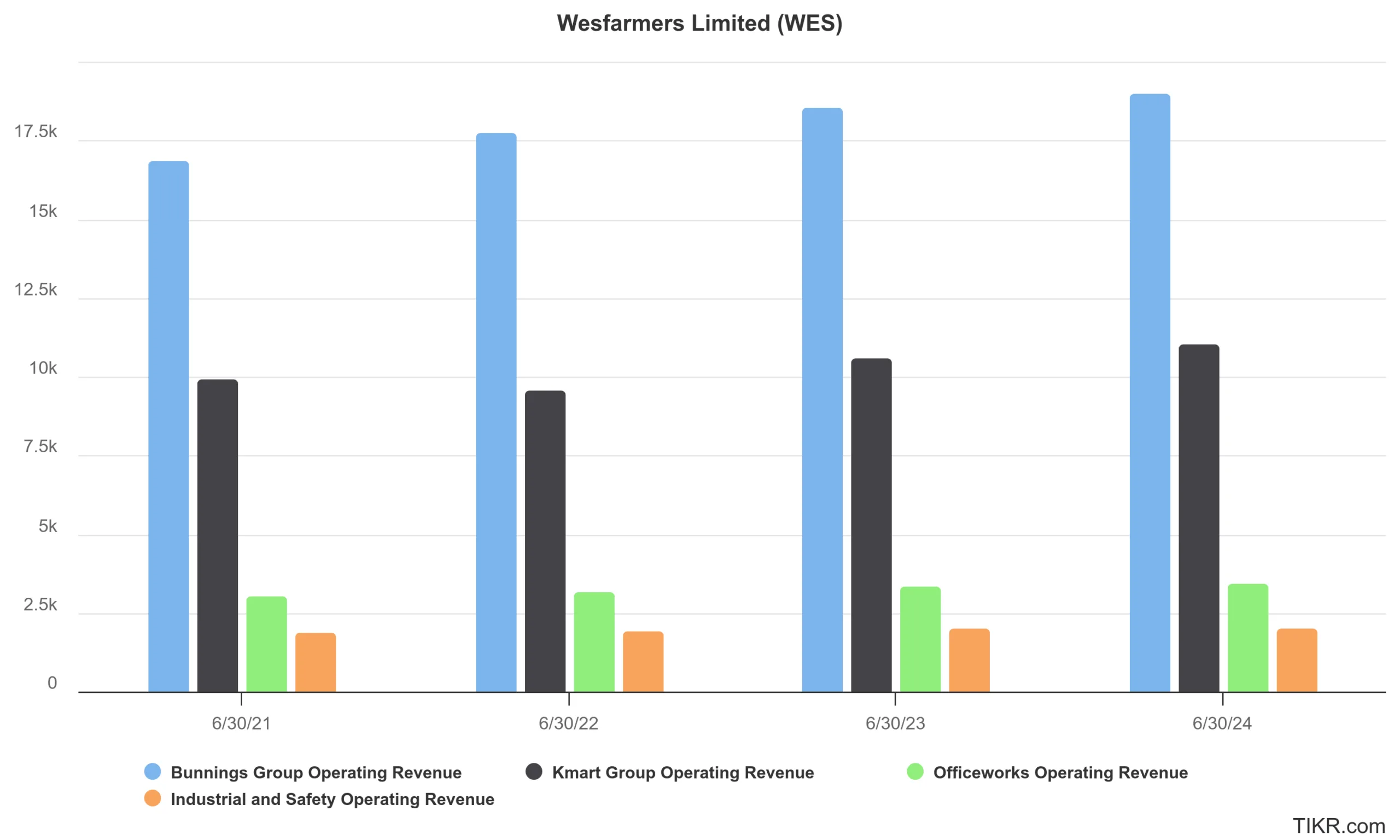

There are fewer, more iconic Australian pastimes than a Bunnings snag.

Couple that with a love of bargains at Kmart and stationery swag from Officeworks, and you begin to build a formidable retail portfolio that stands up in any market. The three retail segments (Bunnings, Kmart & Officeworks) generated ~76% of Wesfarmers’ revenue for FY24. This growth continued in 2024, despite sluggish spending and cost-of-living pressures.

The divisions have a key focus on Aussie households, capturing consumer spend across all stages of life.

For a sign of Bunnings’ dominance, look no further than Woolworths Group Ltd’s (ASX: WOW) failed attempt at competing, with their Masters store rollout. Three years ago, Bunnings was the leading DIY retailer in the Australian market, with a market share of roughly 68%.

Wesfarmers: best-in-class capital allocation

You get what’s on the tin at Wesfarmers. And you don’t have to sift through the website to see its mission:

Wesfarmers’ primary objective is to deliver satisfactory returns to shareholders through financial discipline and strong management of a diversified portfolio of businesses.

The acquisition and spin-off of Coles Group Limited (ASX: COL) was a perfect example of Wesfarmers’ capital allocation credentials.

Wesfarmers acquired Coles Group in 2007 for approximately $22 billion, including Kmart, Target and Officeworks. 11 years of profit and reinvestment in stores, supply chain and IT, funded by Coles, led to a much improved business.

In November 2018, Wesfarmers spun out 85% of Coles before selling the remaining shares in the company for over $20 billion! At first glance, it appears as a loss – but Wesfarmers retained Kmart, Target and Officeworks, plus picked up a ton of profit along the way. That’s some shrewd business!

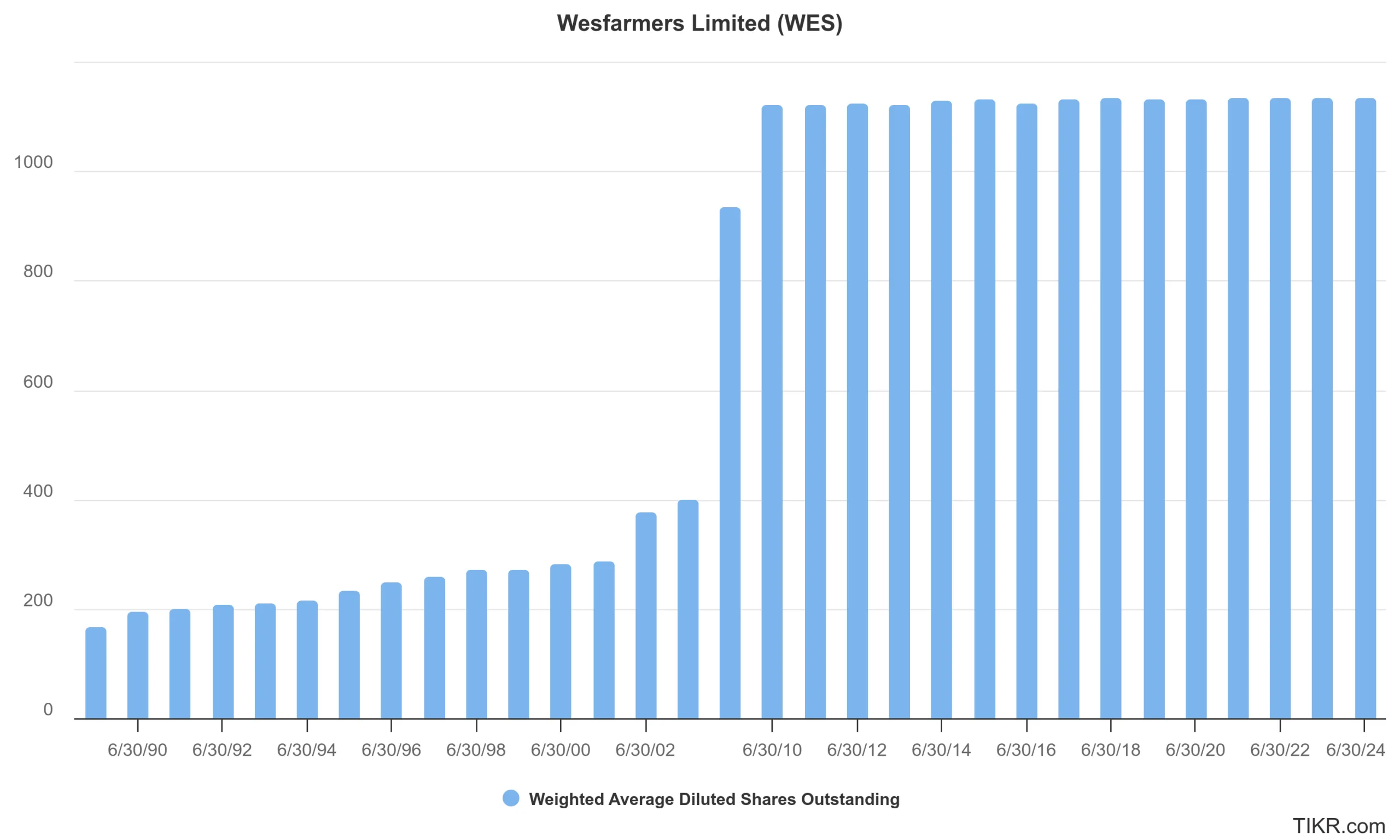

Sticking with its ethos, Wesfarmers has grown shareholder wealth by avoiding ‘returning to the well’. Wesfarmers’ total share count has barely moved since 2009, managing to avoid dilutive acquisitions by selling more shares to investors. This is extremely rare.

This, all while maintaining a consistent return on equity and increasing dividend payments, for several years.

Wesfarmers shares outstanding

Source: The chart above comes from Tikr.com, the best tool for financial data and fundamental analysis.

Source: The chart above comes from Tikr.com, the best tool for financial data and fundamental analysis.

Wesfarmers’ health and energy optionality

Stepping outside a company’s specialty would usually raise a big red flag.

As we’ve touched on, Wesfarmers isn’t your ordinary company.

Wesfarmers acquired API (Australian Pharmaceutical Industries) in March 2022, which gave birth to its health division. It includes 73 company-owned Priceline stores, 396 Priceline pharmacy franchise stores and 89 Clear Skincare clinics. API is also a wholesale distributor of pharmaceutical goods.

There are two areas of focus:

1. Retail

With the division’s overhaul underway, the retail side of API is focused on a refreshed Priceline Pharmacy brand and is exploring new store formats. Updates to Priceline’s Sister Club further complement its e-commerce opportunity. The recent explosion of Chemist Warehouse-turn-Sigma Healthcare (ASX: SIG) shows strong appetite in the market for pharmacy and healthcare.

2. Wholesale

Wesfarmers has an eye on driving growth and efficiency in Pharmaceutical Wholesale. Its investing in supply chain and fulfilment centres, while adding a new platform, aimed at improving the B2B customer experience.

There’s plenty of work ahead, but could health become a ‘second Bunnings’?

Mining & energy

The conglomerate has ventured into commodities, most recently the lithium market through its investment in the Mt Holland mine and Kwinana refinery.

Lithium, a key commodity in the energy transition and electrification of the world, has seen a subdued price.

Fears of oversupply are making it a tough time for lithium producers. With lithium prices currently below production costs, the incentive to produce is muted. Wesfarmers’ lithium business contributed a loss of $24 million, and the company expects its first product at the refinery soon.

While the loss is expected, it’s worth pointing out that the lithium investment complements Wesfarmers’ existing Chemicals, Energy and Fertiliser assets.

Risks for Wesfarmers shareholders

No investment story is too good to be true.

And while Wesfarmers remains well diversified, there are always risks in, and to, each business segment. Divisions can experience downturns at different times, so it’s crucial to be aware of the potential downsides when they may occur.

Things like:

- Downturn in consumer spending, impacting the retail divisions

- Integration difficulties with new ventures, including the significant work going into healthcare.

- Regulatory changes impacting pharmaceuticals

- Put simply, a failure to execute in competitive markets (e.g. the catch.com.au rollout), and/or

- Lithium prices remaining depressed, impacting production and profitability at Mt Holland

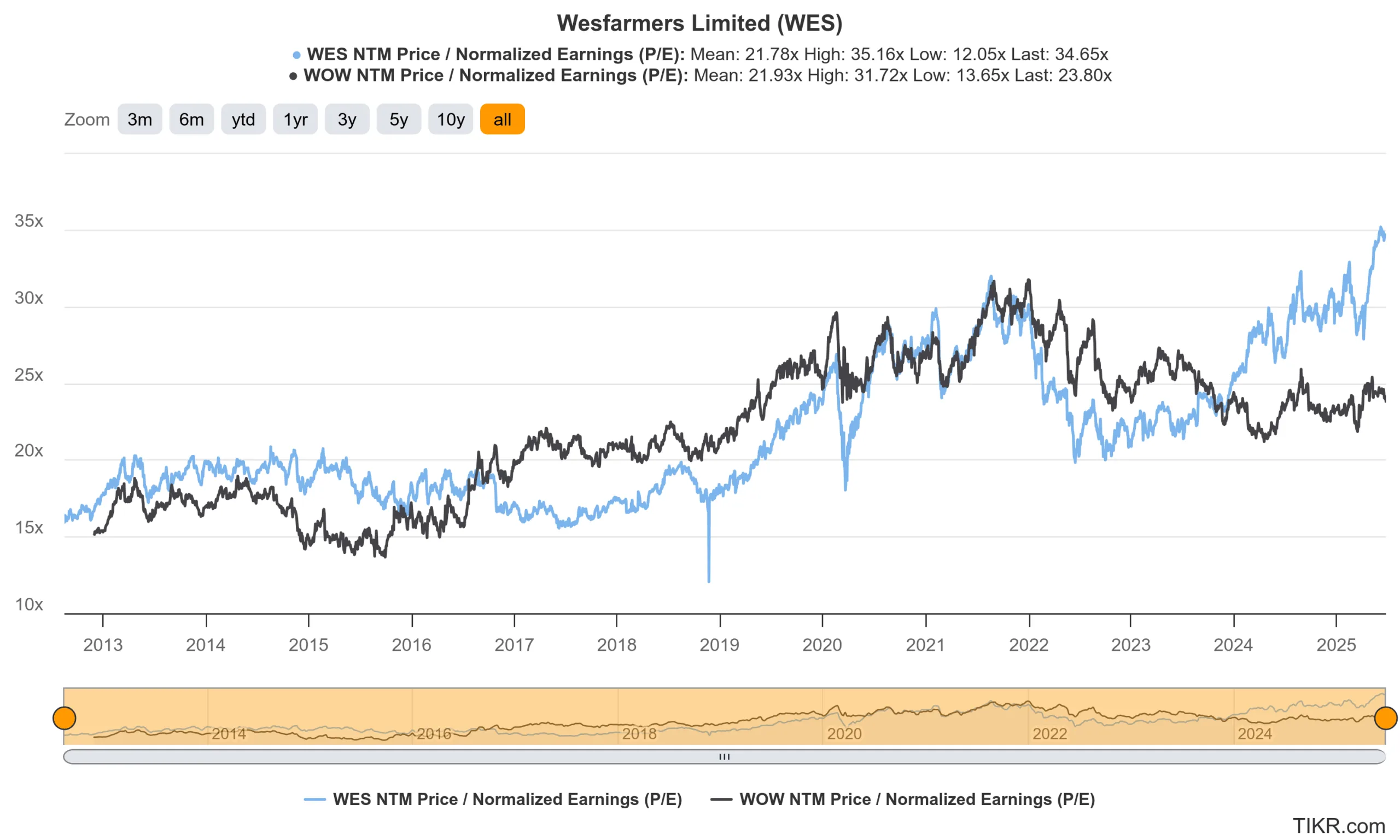

Is the Wesfarmers share price overvalued?

Source: The chart above also comes from Tikr.com, my favourite tool for financial data and fundamental company analysis.

Wesfarmers generated earnings per share of $2.25 in 2024, putting the company on a trailing price-to-profit (P/E) multiple of 37 times.

The Wesfarmers share price is flirting with all-time highs and far from cheap, especially for a company that grew its earnings per share by 3.6% in 2024.

Return on equity (ROE) for the first half was 31.2%, a touch down on the prior period of 31.4% but still an incredible return. It does need to be noted that Wesfarmers carries net debt of $4 billion, which should also be taken into account when considering return on equity.

Beyond being a retail specialist, Wesfarmers is a disciplined capital allocator constantly looking for new growth engines.

At an earnings multiple of 37x, Wesfarmers trades above the market average, but its 31% Return on Equity should keep the stock on our watchlist – and for any other long-term investor reading this, it’s a great play on the private marketplace in Australia.

Therefore, it could complement a rock-solid portfolio of ETFs and/or more growth focused individual shares extremely well.