The stars are aligning for a golden era in private credit.

The recent flurry of interest rate hikes across the globe has returned fixed income to the fore as investors earn meaningful income without needing to take on disproportionate risk. Private credit specifically has acted as a natural hedge against both inflation and higher rates, with most loans originating on floating-rate terms. In fact, private credit today is offering equity-like returns with significantly less risk. As a result, increasing numbers of investors are reallocating their portfolios towards private credit.

The origins of private credit

Private credit, also referred to as private debt or non-bank lending, is an asset class we have been attracted to for some time now. Changes to regulatory standards in addition to the unscrupulous practices revealed by the Royal Banking Commission in 2018 led to the big banks transitioning their loan books away from commercial lending. This left a gaping hole for corporate funding, particularly for loans made to small and medium enterprises that cannot easily issue debt or raise capital.

Interest rates descend

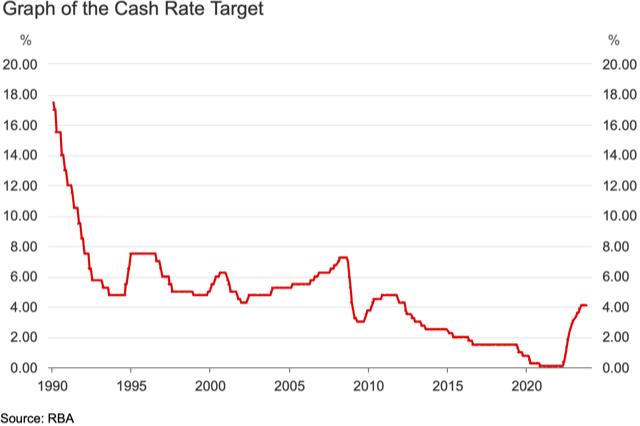

To understand why private credit is set for a golden era, it’s worth reviewing what has shaped markets in recent history. We travel back to 1990 when the cash rate was 17.5% in Australia. This interest rate is deemed to be the “risk-free” rate all other assets, including fixed income, property and shares are priced off.

The commonly accepted belief by the market is the Australian government will never default on their debts and therefore investors need to be rewarded with a higher return for taking on a given amount of risk.

Why accept 7% in shares when you can earn nearly 18% risk-free in the bank? Investors were therefore willing to pay less for assets, and this was reflected in lower prices for homes and shares in public companies.

In subsequent years, interest rates in Australia, and for that matter, the developed world, trended lower. Central banks realised reducing interest rates could be used to bolster the economy, most notably in the early 1990s global recession, the 2008 global financial crisis and more recently in 2020 when the pandemic hit.

The powerful tailwind of lower interest rates proved to be for asset owners. With the returns available from the reserve bank and subsequently low-risk term deposits and government bonds falling, equities and property became much more enticing. For completeness, it should be said interest rates are not the only determinant of asset prices.

But there is little doubt the multi-decade descent in interest rates has only served to amplify returns.

To summarise:

- Interest rates are the “risk-free” rate, as there is a negligible risk of the Australian government defaulting. The interest rate set by the US Federal Reserve (our equivalent of the RBA) is also commonly used.

- Asset prices are inversely correlated with interest rates.

- Higher interest rates generally coincide with lower asset prices, while lower interest rates boost the prices of assets

A tectonic shift

Today, however, we sit at the crossroads of a tectonic shift in financial markets. Central banks across the globe have uniformly increased interest rates to curb inflationary pressures and restore price stability. In Australia, the RBA has increased the cash rate from 0.10% to 4.10% in less than two years.

Howard Marks recently wrote in a memo to clients that this sea change isn’t just another cyclical fluctuation but rather “a sweeping alteration of the investment environment calling for a significant capital reallocation”.

Marks knows a thing or two about debt, as the founder of the world’s largest distressed lender Oaktree Capital.

He argues that higher interest rates are here to stay, and the former era of low interest rates won’t be revisited anytime soon. Subsequently, there will be several flow-on effects including:

- Slower future economic growth

- Profit margin compression

- Increased defaults

- Less reliable asset appreciation

- Reduced access to financing

In other words, after decades of “easy” monetary policy bolstering the valuation of assets, the next era will usher in a new set of leaders. Marks therefore suggests shifting capital away from past winners, such as shares, and into fixed income and credit.

He isn’t alone.

The world’s third-largest credit investor, Blackstone, recently declared the current environment as the best the business has experienced since entering the market in 1998.

“Lending is the most compelling area. It’s an extremely compelling opportunity today in private credit. It is, for sure, some of the best risk-reward we’ve ever seen and within our credit businesses that they’ve seen.”

– Blackstone CFO Michael Chae

The role of private credit

For income and retirement investors, now is the time to consider allocating part of your portfolio to private credit, particularly if they have become overweight equities or property. As Marks concluded, credit can provide investors with:

- Returns that are on par with past equity performance

- Income to fund retirement and cash flow needs

- Significantly lower market volatility that is evident in share prices

The risks credit investors take are quite different to equity risk. Borrowers have a contractual obligation to pay lenders interest repayments. Companies on the other hand have discretion on when and how much dividends should be paid. Moreover, equities are subject to share price gyrations, for example in March 2020 when the benchmark fell over 25%.

With loans offering investors already a 7%+ return, and with the expectation that will increase in the future, credit provides meaningful income to support retirement and lifestyle expenses. Private credit is just one possible allocation within an income strategy and should be held within a diversified portfolio in accordance with your risk profile and financial objectives.

Nonetheless, today represents a wonderful opportunity to reallocate capital towards a growing asset class.

As Marks concludes:

“Unless there are serious holes in my logic, I believe significant reallocation of capital toward credit is warranted.”